Analytics, Banks, Financial Services, Latvia

International Internet Magazine. Baltic States news & analytics

Friday, 03.07.2026, 02:31

Overhaul of Latvia's financial sector supervision continues in the pandemic

Print version

Print versionThe Coronavirus Disease (COVID-19) and its associated health

and economic crisis has shifted attention towards the health, social and

economic crisis response. Major bank lenders have introduced schemes allowing

their customers experiencing temporary financial difficulty to defer their

principal loan payments, and the government has offered support to the banks

via loan guarantees. These domestically focused banks arrived to the crisis

with strong fundamentals. Yet, the pandemic adds to existing challenges for

banks that previously focused on foreign clients and are now transitioning

towards new business models. Latvia's Financial Intelligence Unit (FIU)

highlights that the crisis environment could encourage criminals to exploit the

current situation for financial gain, and the risk of cyber-crime and

suspicious activity could increase during the COVID-19 pandemic1.

However, Latvia's FIU has made clear its commitment to

continue monitoring suspicious transactions, and DBRS Morningstar expects

continued improvement in the area of anti-money laundering, combating the

financing of terrorist, and proliferation financing (AML/CFT/CPF). Latvia's

financial sector regulator (FCMC) has developed strict procedures for

determining ML/TF/PF risk levels at Latvian banks and will individually

supervise financial market participants to mitigate possible adverse effects of

the crisis.

This commentary aims to assess the consequences of the

crisis on the banking sector, highlight the measurable progress made by the

Latvian authorities prior to the crisis in the areas of risk mitigation and

risk monitoring of banks that service foreign clients, and assess plans for

further progress in the coming years.

COVID-19 shock will affect Latvia's segmented banking system in different ways

By way of background, the Latvian banking system is made up

of two groups of banks with traditionally distinct business models. First,

subsidiaries and branches of banks from the European Economic Area, mostly from

Nordic countries, that focus on Latvian clients. Second, non-resident deposit

(NRD) banks that service foreign clients.

Subsidiaries and

branches of Nordic banks

The majority of domestic lending stems from three large

banks: Swedbank, SEB, and Luminor Latvia Branch (previously DNB and Nordea).

Overall risk to the Latvian financial sector from these banks was limited prior

to the COVID shock. At the end of 2019, these largest credit institutions were

profitable, well capitalized, and had high quality of loans. Nonperforming

loans to total loans declined to 5.0% in 2019, according to the IMF.

While banking financials will inevitably be affected by the

COVID-19 crisis, the short-term negative effects of the crisis have been

mitigated in large part by government support to households and businesses. The

moratorium on principal payments of loans to households and non-financial

corporations (up to 12 and 6 months, respectively) has kept non-performing

loans low, at 5.4% as of June 2020, according to the FCMC2

Non-resident deposit

banks

A challenge for Latvia in recent years has been the lack of

transparency of the origins and usage of the non-resident deposits. In 2016,

Latvia began amending laws to tighten AML/CFT/CPF requirements. Those efforts

were accelerated in 2018, after the financial sector was shaken by the

statement of the US Financial Crimes Enforcement Network (FinCEN) regarding

ABLV Bank and its subsequent self-liquidation. In 2019, a separate NRD bank,

PNB Banka, lost its banking license after it failed to raise additional capital

to continue the process of changing its business model.

DBRS Morningstar considers the COVID-19 crisis ought not to

divert attention from progress made on financial crime. Prior to the crisis the

government implemented various AML/CFT/CPF measures and procedures to

strengthen risk monitoring and mitigation of NRD banks. Below are several

indicators meant to measure the progress.

Risk Mitigation:

reduction of high-risk customers and increase in penalties

Recent legislation forced banks servicing foreign clients to

find a viable alternative to their business model, causing NRD banks to scale

back their operations. The business volume of NRD banks and their deposit base

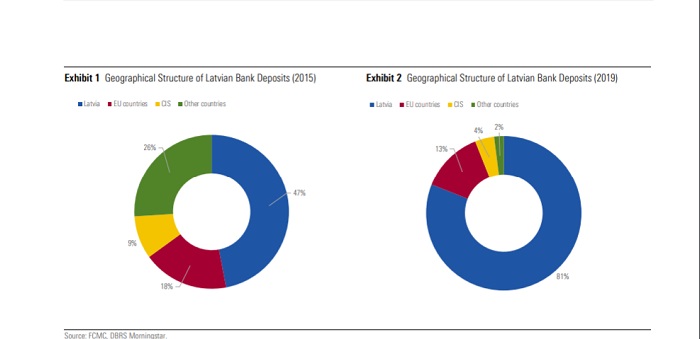

have shrunk significantly. In 2015, over 50% of deposits in the total Latvian

financial system were from nonresidents. By 2019, foreign client deposits

declined below 20%.

Perhaps more importantly, there has been a compositional

change of NRDs remaining in the Latvian banking system. Deposits from EU

countries now represent most of the NRDs. Foreign deposits from customers based

in non-EU jurisdictions - considered more likely to pose ML/TF/PF risks -

amounted to 35% in 2015 (See Exhibit 1). By 2019 and underscoring a dramatic

shift, foreign deposits from customers based in non-EU jurisdictions (CIS and

Other Countries in the Exhibits) constituted roughly 6% of total customer

deposits (See Exhibit 2).

Risk is also mitigated by the increase in on-sight

inspections and the increased propensity of bank fines and seized assets. All

banks have undergone money laundering risk assessment, and 17 fines worth 18.7 mln

EUR were imposed on penalized banks from 2016 to 2019. In the first three

months of 2020 alone, the FIU froze EUR 160 mln in assets.

Risk Monitoring:

upskilling of regulatory personnel and IT solutions

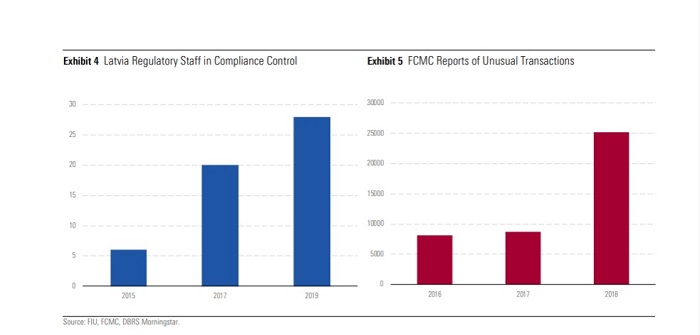

Monitoring procedures have been improved in various ways. To

begin, Latvia has increased the staff dedicated to financial supervision. The

number of FCMC compliance control staff in the area of AML/CFT/CPF has

increased from only 6 employees in 2015 to 28 in 2019 (See Exhibit 4). The

growing staff has allowed for an increase in on-site inspections. In 2018 and

2019 all high risk banks were subjected to the FCMC on-site inspection,

previously a less frequent occurrence.

The number of prosecutors participating in specialized

anti-money laundering training has also increased in recent years. In 2019, 330

prosecutors participated in various AML training schemes, up from 193 in 2018.

The increased number and upskilling of the staff promoted more effective

dialogue between the regulator, the financial sector, and law enforcement

bodies – allowing for cross-border dissemination of suspicious transactions. As

a result, 59 criminal cases were brought before the court in 2019, up from 23

in 2018 and 10 in 2017.

The FCMC has also implemented information technology

solutions that analyze unusual cash flows to help increase the efficiency of

monitoring AML/CFT/CPF risk. Due to the improved IT tools and the larger FCMC

staff, the number of reports on unusual transactions increased to 25,170 in 20183, nearly a threefold increase from the year

earlier (See Exhibit 5).

The difficult work of

overhauling Latvia's banking sector is far from complete

Many banking sector challenges remain, including (1)

strengthening the capacity of law enforcement authorities to handle money

laundering cases and (2) managing the transition of NRD banks to new business

models.

In its 2020 semester country report, the European Commission

(EC) states that Latvia should strengthen beyond the initial gains the dialogue

between the regulators, financial sector participants, and law enforcement

bodies. In this regard, Latvia needs more advanced training of judicial

stakeholders in order to improve the quality and effectiveness of prosecuting

money laundering cases, according to the EC.

The priority of the FCMC is to remain vigilant that NRD

banks are effectively reorienting their business models away from servicing

foreign clients. The full transition will take time and come with a cost. The

downsizing of NRD banks poses refinancing and liquidity risks at a time when

these banks have seen the quality of their foreign loan portfolio deteriorate.

Stress in the NRD sector has had limited spillovers to the domestic economy and

caused no reputational damage to banks focused on domestic clients. The stress

nonetheless does point to the scale of the challenge for Latvia in addressing

its legacy banking sector issues.

DBRS Morningstar considers favourably the speed and urgency

with which the Latvian authorities are overhauling the supervision of its

financial sector. Strengthening of the financial sector is a key driver of DBRS

Morningstar’s Latvian ratings. Visit dbrsmorningstar.com for details about DBRS

Morningstar's ratings drivers for Latvia.

- 28.01.2022 BONO aims at a billion!

- 25.01.2021 Как банкиры 90-х делили «золотую милю» в Юрмале

- 30.12.2020 Накануне 25-летия Балтийский курс/The Baltic Course уходит с рынка деловых СМИ

- 30.12.2020 On the verge of its 25th anniversary, The Baltic Course leaves business media market

- 30.12.2020 Business Education Plus предлагает анонсы бизнес-обучений в январе-феврале 2021 года

- 30.12.2020 Hotels showing strong interest in providing self-isolation service

- 29.12.2020 В Латвии вводят комендантский час, ЧС продлена до 7 февраля

- 29.12.2020 В Rietumu и в этот раз создали особые праздничные открытки и календари 2021

- 29.12.2020 Latvia to impose curfew, state of emergency to be extended until February 7

- 29.12.2020 18-19 января Наталия Сафонова проводит семинар "Управленческий учет во власти собственника"

«The Baltic Course» Is Sold and Stays in Business!

«The Baltic Course» Is Sold and Stays in Business!