Analytics, Direct Speech, Forum, Investments

International Internet Magazine. Baltic States news & analytics

Tuesday, 28.04.2026, 13:00

Foreign Direct Investment and Business Development

Print version

Print version |

|---|

Many

empirical studies show that long-term economic growth can be driven primarily

by fixed investment that is influenced mostly by national saving. In particular,

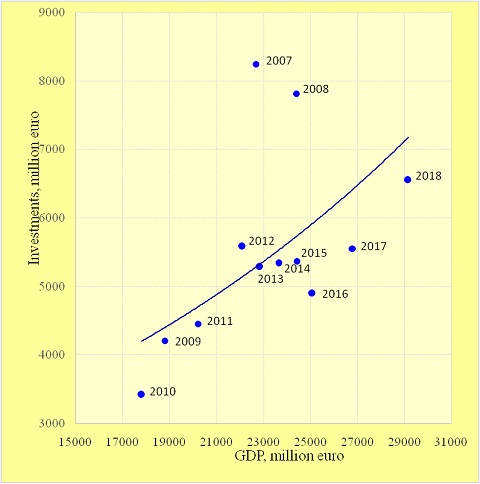

Figure 1 highlights the underlying trend in the relationship between fixed

investment and GDP is positive for the Latvian economy. It is necessary to encourage

investment activity as one of the driving forces of achieving sustainable and

inclusive economic growth in Latvia.

Fig.1.

Investment and GDP Growth in Latvia

Source. Eurostat data.

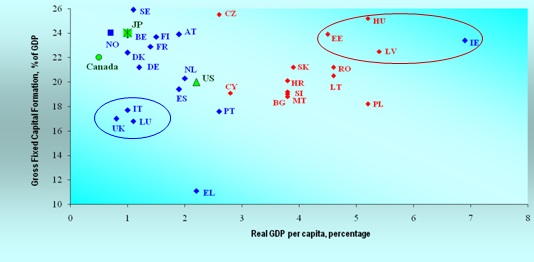

Empirical

evidence revealed the existence of this relationship for other EU countries as

well. For example, substantial differences in levels of gross fixed capital

formation and real GDP per capita between Latvia, Estonia, Hungary, Ireland on

the one hand and the United Kingdom, Italy, Luxembourg on the other hand indicate

that the higher investment activity, the greater real GDP per capita growth

rate, as depicted in Figure 2. Relative to these countries of Old Europe such

a regularity can also be

considered for Spain, the Netherlands, the USA, France, Finland, Austria, the

Czech Republic, Cyprus, Croatia,

Slovakia, Romania. Besides, this positive trend is also observed

regarding Canada, Norway, Japan, and Sweden. Nonetheless, despite the cross-country differences in fixed

investment levels between Sweden, Japan, Belgium, Denmark, Germany, Italy, and

Luxembourg, percentage of real GDP per capita remains the same in these

countries. Similarly, such variances there are between Norway and the United Kingdom. Meanwhile, another

trend explicitly appears, when some countries like Italy, Luxembourg, Greece,

Spain, the Netherlands, the USA, Portugal, Cyprus, especially Bulgaria, Malta,

Slovenia, and Poland in terms of a lower gross fixed capital formation

percentage achieved a much higher real GDP per capita percentage in comparison

with Canada. Taking into account the cross-country differences in rates of

gross fixed capital formation and real GDP per capita it should be noted that fixed

investment is not the only or main source generating economic growth as it is

shown in the empirical studies in this area.

Fig.2.Investment and Real GDP per capita, 2018

Source. Eurostat data.

Under the

conditions of increasing openness of national economies and international

competition foreign direct investment (FDI) became a key driver of

competitiveness and business development and consequently can significantly contribute

to long-term sustained economic growth. It is worth noting that from the

standpoint of investors’ future intentions and possible investment trends

dynamics, a crucial factor driving FDI decisions is investor confidence.

According to the data of the Global Business Policy Council in 2019 the highest

FDI confidence index is in the

USA (2.10), Germany (1.90), and Canada (1.87). In addition to Germany, among

European countries the top 10 on this index includes also the United Kingdom in

the rankings (4), France (5), Italy (8). As shifts in sectoral FDI flows especially

to high-tech manufacturing in developed markets show, FDI can affect economic

performance across industries and firms to a greater extent through

international technology transfer and R&D projects.

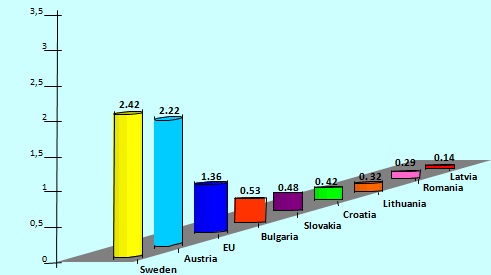

Fig.3. R&D Expenditure in the Business

Enterprise Sector, % of GDP, 2017

Source. Eurostat data.

However,

such an indicator of

increasing the stock of knowledge as R&D expenditure performed within

the business enterprise sector in the EU indentified challenges for promotion

of knowledge-based long-term economic growth in countries of New Europe, as

illustrated in Figure 3. The

highest R&D intensity as a percentage of GDP in the EU is achieved in

Sweden (2.42%), Austria (2.22%) relative to the EU average – 1.36%. Hence,

Sweden and Austria are innovation leader and strong innovator, respectively. While

this indicator in Bulgaria is 0.53%, Slovakia – 0.48%, Croatia – 0.42%,

Lithuania – 0.32%, Romania – 0.29% and the lowest indicator is in Latvia –

0.14%.

The fastest growing economies in Asia have benefited from foreign direct investment (FDI)-oriented

innovation activity, increasing substantially their innovative capacities that

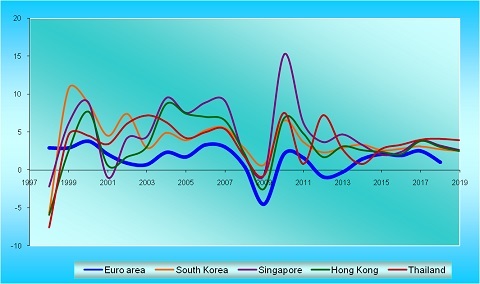

will be a crucial determinant of global competitiveness. Figure 4 displays that

real GDP growth rate in South Korea, Singapore, Hong Kong, and Thailand considerably

exceeded the level of this indicator in the Euro area.

Fig.4. Real GDP Growth

Source. Eurostat,

UNCTAD data.

Moreover, according to UNCTAD data the Asia-Pacific region received

significant especially greenfield FDI inflows to the manufacturing and services

sector. In particular, China becomes an investment destination for FDI in high

value-added industries and Thailand aims to attract more FDI in

technology-based manufacturing and services. By data of ASEAN Investment Report

(2018) the ASEAN telecommunication industry will have continuing and increasing

FDI inflow in the development of ICT infrastructure in the long run. Besides, East

Asia and the Pacific become one of the most improved regions with their

competitiveness performance upward trend (+1.78%) in the world. Economies of this

region perform better than Europe and North America on the Product market and

the Financial system pillars of the Global Competitiveness Index. In such

dimension as the ICT adoption pillar the East Asia and the Pacific region economies

actually have achieved a similar level of performance like Europe and North

America. While the positive percentage change of this region performance in ICT

adoption (4.4%) is greater than the pace of change (3.7%) in Europe and North

America. Furthermore, in terms of changes in competitiveness performance there

are also cross-regional differences in the Innovation capability pillar, most

notably for economies of East Asia and the Pacific with significant improving

(+2.0%) versus the unchanged trend on this pillar in Europe and North America. These

disparities indicate that competitiveness of the East Asia and the Pacific

economies is driven mostly by the progress in ICT adoption, financial system,

innovation capability and improving macroeconomic stability that contributed to

a favorable investment environment. Despite sharp declining global FDI flows mainly in developed countries and

transition economies in 2018, nevertheless according to the annual data of

UNCTAD, FDI inflows to developing Asia rose by 4 percent to $512 billion, especially

in China, Hong Kong (China), Singapore, Indonesia as well as India and Turkey. Receiving

39 percent of global FDI inflows, Asia became the largest region with a growing

share of FDI in the world.

The overall positive trend also appears in the relationship

between shares of extra-European FDI inflows and EU GDP. More specifically,

this effect reflected in a steady and higher growth dynamics for the Netherlands, Spain, Italy, France,

the United Kingdom, and Germany. Noteworthy, the highest percent of EU FDI is concentrated

in science-intensive industries like manufacture of computer, electronic

and optical products as well as in services sectors in terms of number of

foreign firms and share of foreign assets in the sector. Besides, these

industries and sectors, especially R&D, IT services, financial services and

insurance have the highest number of mergers and acquisitions deals and also the

highest concentration of foreign investment as to the value of the greenfield

projects. At the same time, the growing share of foreign assets is greater in

the sector of mining and quarrying. Another

peculiarity of FDI in the EU is

high inward FDI stocks, mainly in small countries as Luxembourg, Malta, Cyprus,

the Netherlands, Ireland, and Belgium. Furthermore, namely, the Netherlands and Cyprus, like Germany, show

maximum positive changes in total extra-EU inward FDI stocks. Similarly,

such a trend there is relative to change in inward extra-EU FDI flows that also

indicates maximum percentage points for the Netherlands and Cyprus,

like the United Kingdom.

The empirical

estimates of various sectoral trends of FDI in the international

investment landscape highlighted that the size and growth rate of the economy

are not significant among fundamental determinants of FDI inflow in European

countries. The major trends in actual FDI flows in the world’s most dynamic

economies point that investor preferences and the investment opportunities are

influenced to a greater extent

by taxation, the technological and innovation capabilities, conducive macroeconomic

environment, regulatory transparency, digital infrastructure, level of

openness, skilled workforce, and integration into international value chains

that can contribute to companies competitiveness and profitability.

«The Baltic Course» Is Sold and Stays in Business!

«The Baltic Course» Is Sold and Stays in Business!