Analytics, Crisis, EU – Baltic States, Financial Services, Round Table

International Internet Magazine. Baltic States news & analytics

Tuesday, 23.06.2026, 03:50

Risk management: concept, positioning and priorities

Print version

Print versionAt a time of present financial and economic crisis both lay people and authorities are asking the same question: how did it happen that the coming threats could not predicted or at least foreseen. It is true that RM was addressed already two years ago, e.g. Special Report on RM in Financial Times on May 1, 2007. Already then it made a couple of interesting conclusions: first, modern economic development created a new set of risks (more complicated and system-like), and, second, an optimal market based RM shall be installed for a market-based valuation of bank’s credit portfolio and “public” assessment of national development models.

The author attempts to show that modern crisis has a systematic character, which has made it extremely difficult to predict and properly assess, hence the present outcomes. However some analysis can make the future risk assessment a more foreseeable and predictable task: the successful approach would challenge conventional thinking.

Main concept and alternatives

Risk management (RM) is generally understood to mean “a process for alerting senior executives to unexpected problems, as well as clear procedures for identifying and managing all sorts of foreseeable risk” (bold mine, EE). [S. Grene. Managers fail to control hazards, -Financial Times, Weekly review of the fund management industry, April 6, 2009, p.15].

Three aspects of modern RM concept are important in the mentioned definition, if transferred into functions; these aspects are generally common to other publications on management and marketing. [e.g. International Marketing: a global perspective, 3rd ed. Muhhacher H., Leihs H., Dahringer L., -Thomson Publ., UK. 2006].

- First RM’s function is to warn or alert senior executives on possible risks and unexpected problems facing the business or/and public entities;

- Second RM’s function is to identify foreseeable risks, and

- Third RM’s function is to manage all sorts of such risks, foreseeable of course, in the first place.

As to the first “conceptual function”, RM quite seldom makes any sensible alerts of expected “situational character”. Even when it does, these alerts are not dealt with accordingly, as happened with the present crisis: the alerts for financial sector have been in the agenda already for more than two years ago without managerial outcomes.

As to other two functions, the process of crisis identification and management becomes a function of political, economic and legal prerequisites, which is too difficult to alter presently.

Financial crisis gave the first alert

We can see presently that there is much more focus on RM than two or three years ago. The crisis has shown that we are facing rather new type of risks. For example, liquidity risk as a major problem for asset management that had not been in the risk models before. Besides, increasing use of complex financial instruments requires more sophisticated RM; and global banking system exposed various countries to new operational and systematic risk. This complicated sphere is clearly seen in the Yahoo website: there are more than 473 mln (!) hits on “risk management”, more than for such key words as “peace” with 116 mln and “freedom” with 96,5 mln hits (data from end of April 2009).

Financial sector is more active presently to clarify the fact that managers failed to control risk hazards. Thus, Peter de Proft, director general of the European Fund and Asset Management Association argued that the asset industry “had outstripped its own ability to manage risk”, being largely short-sighted. Naturally, that most focussed on RM are, all kind of investors.

Various surveys conducted recently have shown that poor strategic understanding for large financial loses are generally blamed during last two years; RM was not treated as an important sector in organisations.

More than that, RM status has often declined without plans for future changes (S. Grene, op citation in Financial Times, 6 April, 2009, p.15). In this article, Steen Thomsen, a professor at Copenhagen Business School argued that RM was presently in a decision vacuum, due to the fact that the main source of risk advice came from public regulatory authorities, especially in asset management.

Keeping in mind that banking and financial sectors are quite separate from important public decisions, it would take a long time for regulators to respond, it seems.

However, one step in a process of regulatory reform has been taken: Committee of European Securities Regulators recently released “consultation statement” on RM principles for Ucits, European retail fund structure. The next move would be to install the RM function into financial service industry.

Neelie Kroes, EU Commissioner for competition said recently that “in recent years, the banking system and financial investors wanted too much, too quickly. Too much risk was taken with other people’s money, with dramatic systemic consequences: more than €3,000bn ($3,940bn) of other people’s money – that of taxpayers – has now been used to pull banks out of the hole they dug for themselves” (-Financial Times, April 27, 2009).

Surveys in different countries and organisations have shown the RM’s low priority despite the financial and economic crisis. The abovementioned “decision vacuum” in RM at present can be attributed to the fact that the main alerting body of risk advice comes from either national or/and international regulatory authorities.

Risk hazards: Union’s role and function

Risk assessment has been an integral part of all study programs in management courses. However it did not prevent the financial sector from collapse. The main reason behind the problem was introduction of numerous financial instruments with all the complexities of their functioning. Investors could not figured out how these schemes were managed; and often the “operators” could not make it either.

Huge liquidity inflow into banking sector made it questionable for the EU competition rules to deal with such state aid on a massive scale. Thus, in recent years the banking system and financial investors worked hard striving for quick profits.

The EU Commissioner for competition met almost every European big bank chief executive since the financial crisis began. Quite remarkable fact, she argued, that most of them were in denial, considering that “their” bank had no problem – only others did. Such “denials” -not just from bankers’ side– suggest we need only focus on stability, setting competition rules aside. European banks cannot set aside the Union rules, said Neelie Kroes, pointing out the this was the “muddled thinking”. Instead, stability should have come first in order to safeguard citizens’ savings and proper financing the economy. Without taking into account control hazards, present stability has come at a very high price.

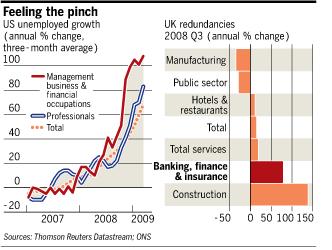

On the table below it is seen that the crisis has hit hard banking sector and construction in Europe (in the UK, as an example) and management/financial sector (e.g. in the US).

The Commission has come with the suggestion in April 2009 for the member states when approving national aid to rescue banks and maintain lending to the real economy. The European Commission imposed conditions to ensure co-ordination between member states, to enforce the European Union’s single-market rules and to preserve free competition among banks, both now and after the recovery.

European and American responses

It is clearly seen that continental Europe was less exposed to financial crisis: it has been less dependent on mortgage-based securities. That gave the banks a vision that they could ride out of the crisis. Too many leaders in the EU thought that they did not need a Europe-wide solution to the crisis. However the amounts involved in various rescue packages are enormous: IMF expects write-downs by banks in the eurozone only to reach $750 bn in the next two years, plus $200 bn in the UK alone [Financial Times, Editorial –A single stress test, 27.04.09].

Europe’s delayed involvement is explained by the fact that most of its financial intermediation is still done by banks, not by a shadow banking system. Securitised lending is a small part of total credit. But since recession hit the real economy, European banks suffered great losses and IMF’s conventional loans expected to cover most of these losses.

Accounting rules also allow banks to avoid writing down losses on loans until they materialise. But that does not remove their incentive to de-leverage, if they expect those losses to come eventually. Policymakers are therefore right to worry that credit is being withheld from the wider economy. To prevent a credit contraction in a recession, banks must be forced to hold enough capital to sustain lending.

Hence, the need for capital adequacy audits or “stress tests”, argued the Commission. In Europe’s integrated banking market, such tests – and the consequences for banks that fail them – should be designed in common and applied consistently in different countries. A patchwork of national solutions inevitably distorts competition and ignores their negative effect on neighbouring countries.

Neelie Kroes, EU competition commissioner, valiantly tries to enforce a level playing field; but subjecting national policies to state aid rules is no substitute for a common policy. There will be political obstacles to a common approach in the EU as long as member states retain final responsibility for recapitalising insolvent banks. That does not alter the hard fact that only a common approach will work.

Private equity response to systematic risk

Simon Walker, chief executive of the British Private Equity and Venture Capital Association warned that proposed EU direstive on alternative investment fund managers published by the European Commission in April 2009 was absurd. [Europe’s plan threatens private equity, -Financial Times, April 29 2009].

“What is being suggested would bring a huge number of mid-market private equity houses into a new and onerous regulatory regime and in so doing would also capture many hundreds of portfolio companies”, writes S. Walker.

The justification for intervention is the “systemic risk” for which alternative investment fund managers are allegedly responsible. Some have indeed been accused of playing that role, such as the hedge funds. But private equity has not been charged with adding to system risks, either in this proposal or a series of other international reports. There is no rationale for the Commission to intervene against private equity. Yet, if the EU investment directive were to become law, it would have a dramatic and damaging impact on the industry.

There is a deep irony in this: private equity is well positioned to assist Europe’s economic recovery. It has more than €114bn ($150bn) in funds in Europe ready to deploy in acquisitions. It has already played an important role in rescuing ailing and failing companies in Britain, as well as in Germany and Sweden. It is force for good which European political institutions should be encouraging rather than threatening with intense regulation, argued S. Walker.

There are a number of detailed provisions which will adversely affect the larger buy-out houses. The most striking feature of the EU proposal, nonetheless, is the effect it would have on the mid-market sector and pure venture capital companies which expand beyond a certain size. The direct additional expenditure would be in a range of £25,000-£30,000 per company in the portfolio, with the sizable indirect additional costs. This measure would thus heap utterly unwarranted costs on parts of the economy which should be left free to create real value and would do so at the worst possible time.

The scheme seems unfair to some experts arguing that it will have a severely anti-competitive bias. A huge range of privately controlled companies will be excluded by these regulations, while those owned by private equity will be compelled to obey them. It will also create a vast and unwanted burden for the regulators, concluded S. Walker. The FSA would be obliged to police a swathe of companies far smaller than its normal customers, for which it lacks the in-house expertise and in the knowledge that there is nothing to be won in terms of enhanced economic stability.

The British interests often run across those on the Continent: almost 60 per cent of the European private equity industry is located in the UK and about 40 per cent of European portfolio companies which are presently hit by the crisis are owned by private equity houses based in the UK. [Financial Times, 29.04.2009].

A “regular British response” is to resist the EU initiatives but such British government steps would be profoundly bad for British business. Some say that it is insane to imply that the financial crisis means thorough regulations for small and big -publicly quoted- companies. But this is precisely what will happen if ministers in sectoral economies would not find an adequate solution.

Global risk assessor

As a radical solution to the global and national RM issues policymakers are increasingly calling for the creation of an early warning system to prevent future financial, economic and other kind of crisis. It is, in fact, unclear as to who would operate such a system and how it could work.

However, some economists have made some suggestions: thus, Nicholas Stern’s comment, former chief economist if the EBRD and World Bank, deserves a special attention.

Mr. Stern suggested a “global risk assessor” to detect and manage crisis promptly, authoritatively and independently of “big countries and important economies”. [Stern S. The world needs an unbiased global risk assessor”, -Financial Times, March 25, 2009, p.9].

Unbiased assessment of global economic system’s stability is based on two requirements - it must be independent of: a) existing international financial institutions (which is theoretically possible), and b) important economies (which is difficult to imagine).

«The Baltic Course» Is Sold and Stays in Business!

«The Baltic Course» Is Sold and Stays in Business!