Analytics, Financial Services, Labour-market, Latvia, Markets and Companies, Wages

International Internet Magazine. Baltic States news & analytics

Saturday, 27.04.2024, 05:54

Hourly labour costs in Latvia grew by 36 cents in Q4

Print version

Print version

Labour cost growth in the 4th quarter of 2014 was mostly affected by rise in wages and salaries of 7.2%, while other hourly labour costs increased by only 1.5%.

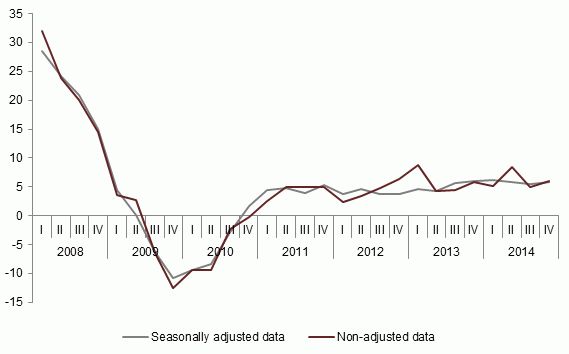

|

| Changes in hourly labour costs over the corresponding quarter of the previous year, % |

Data source: Central Statistical Bureau of Latvia

The most notable increase in hourly labour costs was recorded in health and social work activities – of 9.7%, in real estate activities – of 9.6%, in construction – of 9.2%, in administrative and support service activities – of 8.2%, and in public administration – of 7.3%.

In all these sectors except real estate activities, labour cost growth was caused by increase in both – wages and salaries, and irregular premiums and bonuses. Regular wages and salaries in real estate activities grew by 13.1%, while irregular premiums and bonuses declined by 24.4%. In construction and real estate activities growth in hourly labour costs was also promoted by decrease in the number of hours worked – of 2.2% and 0.1%, respectively.

Changes in hourly labour costs and wages in the 4nd quarter of 2014 by economic activity (seasonally non-adjusted data, EUR)

|

|

Hourly labour costs |

of which hourly wages and salaries |

||||

|

Q4 2013 |

Q4 2013 |

Changes, % |

Q4 2013 |

Q4 2014 |

Changes, % |

|

|

Total (B-S) |

6.18 |

6.53 |

6.1 |

4.89 |

5.24 |

7.2 |

|

Mining and quarrying (B) |

7.90 |

7.98 |

1.1 |

6.25 |

6.38 |

2.1 |

|

Manufacturing (C) |

5.83 |

6.13 |

5.2 |

4.60 |

4.91 |

7.0 |

|

Electricity, gas, steam and air conditioning supply (D) |

8.42 |

8.87 |

5.3 |

6.29 |

6.77 |

7.7 |

|

Water supply; sewerage, waste management and remediation activities (E) |

6.13 |

6.31 |

2.8 |

4.85 |

4.99 |

2.8 |

|

Construction (F) |

5.76 |

6.29 |

9.2 |

4.64 |

5.09 |

9.9 |

|

Wholesale and retail trade; repair of motor vehicles and motorcycles (G) |

5.36 |

5.63 |

4.9 |

4.27 |

4.53 |

6.1 |

|

Transportation and storage (H) |

6.80 |

7.17 |

5.4 |

5.41 |

5.74 |

6.2 |

|

Accommodation and food service activities (I) |

3.88 |

4.16 |

6.9 |

3.13 |

3.36 |

7.6 |

|

Information and communication (J) |

9.65 |

10.28 |

6.5 |

7.66 |

8.29 |

8.3 |

|

Financial and insurance activities (K) |

13.12 |

13.85 |

5.6 |

10.06 |

11.06 |

9.9 |

|

Real estate activities (L) |

5.09 |

5.58 |

9.6 |

4.06 |

4.51 |

11.3 |

|

Professional, scientific and technical services (M) |

7.03 |

7.24 |

3.0 |

5.82 |

6.08 |

4.5 |

|

Administrative and support service activities (N) |

5.34 |

5.77 |

8.2 |

4.31 |

4.71 |

9.2 |

|

Public administration and defence, compulsory social security (O) |

8.17 |

8.76 |

7.3 |

6.39 |

6.80 |

6.5 |

|

Education (P) |

5.12 |

5.43 |

5.8 |

4.06 |

4.34 |

7.0 |

|

Health and social work (Q) |

5.42 |

5.95 |

9.7 |

4.34 |

4.78 |

10.1 |

|

Arts, entertainment and recreation (R) |

5.44 |

5.39 |

-0.7 |

4.34 |

4.32 |

-0.4 |

|

Other service activities (S) |

4.80 |

4.87 |

1.5 |

3.96 |

4.06 |

2.6 |

Both seasonally adjusted and seasonally non-adjusted data are available in the CSB database section Labour costs.

1 Differences in the number of calendar days and seasonal influence have been averted.

Explanations

Hourly labour costs include gross wages and salaries and other labour costs.

Wages and salaries are regular and irregular direct wages and salaries – basic salary (monthly, wage), payment for time worked or job completed, regular and irregular premiums and bonuses, payments for days not worked (vacation and other days not worked), state mandatory social insurance contributions paid by the employees, and personal tax. In line with the European Union (EU) regulatory enactments, when compiling data on labour costs, wages and salaries also include remuneration in kind (goods and services provided by the employer to employees free of charge or at a lower price, living quarters, mobile telephone, transport compensation etc.). Other labour costs include statutory social security contributions payable by the employer, employers’ contractual and voluntary social security contributions (additional pension insurance contributions, health and life insurance contributions etc.), support payments from the employer, awards, gifts, payments for sick list A, severance pay, entrepreneurship state risk duty.

Hourly labour costs are calculated dividing the sum of labour costs by the number of hours worked.

According to the EU regulatory enactments, hourly labour costs and changes thereof in this publication have been calculated for sectors B-S of the Statistical Classification of the Economic Activities (NACE) Rev. 2.

Indicator changes have been calculated from not rounded values.

«The Baltic Course» Is Sold and Stays in Business!

«The Baltic Course» Is Sold and Stays in Business!