Banks, Covid-19, Direct Speech, Economics, Latvia

International Internet Magazine. Baltic States news & analytics

Sunday, 05.07.2026, 19:54

Eight-toothed spruce bark beetle and two-toothed crisis in manufacturing

Print version

Print version |

|---|

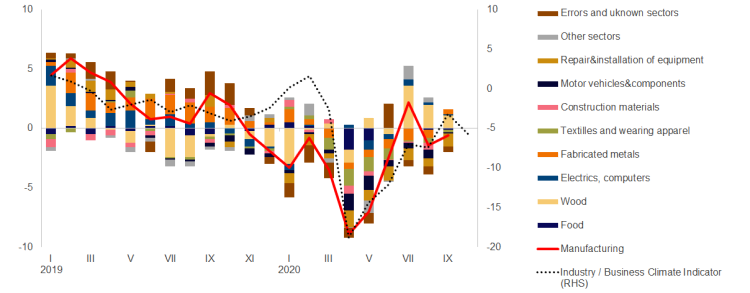

Why "kind of good"? The growth was mostly driven by the wood industry, the largest subsector of manufacturing (see Chart 1). Positive contribution was also seen in the manufacture of machinery and equipment n.e.c., manufacture of rubber and chemical products, and some other subsectors. A large part of sectors, however, have failed to reach their pre-crisis production volumes.

The wood industry fared pretty badly last year. It faced heaps of challenges, e.g. over-saturated supply of wood due to bark beetle damage, low prices of wood, demand issues in selected segments and other problems. With higher wood prices and smaller bark beetle damage, this year has been considerably more favourable. Thanks to our folk deities Mother of Forests and Father Thunder, or just a coincidence of circumstances, the capability of so important a sector to increase its turnover during the crisis has been particularly beneficial.

However, it is not quite true that the entire wood industry is thriving now. According to the sectoral association, the basic products are doing well indeed and the demand for selected products considerably exceeds the production capacities of many companies, while for by-products, such as wood chips, sawdust and pulpwood, this period is difficult.

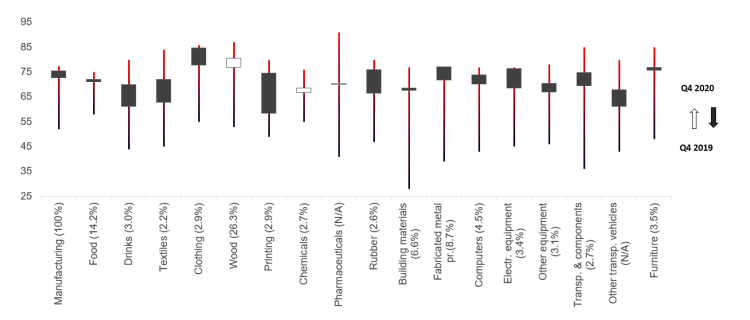

In the fourth quarter (the survey is conducted in the first month of the quarter, i.e. in this case in October), capacity utilisation in manufacturing shows further improvement, while overall it is still below the level seen last year. With respect to these data, wood processing also demonstrates higher capacity utilisation than a year ago, so do chemicals, and pharmaceutical products have slightly higher capacity utilisation. In other sectors, the situation is not so positive (see Chart 2).

According to monthly surveys, the industrial confidence indicator deteriorated in October, suggesting that the above production capacities could have already been harmed by the second tooth of the crisis, i.e. the second wave of the COVID-19 pandemic, which is a much more hostile force than the eight-toothed spruce bark beetle which has been slightly slower this year. Therefore, despite the strengthening of wood processing, it is rather unlikely that the production volume declines could be prevented in the coming months. Both domestic and external demand is going to weaken, and the numbers of employee quarantine and company downtime cases will expand. But let us try to remain optimistic, spring will bring everything in blossom again.

- 28.01.2022 BONO aims at a billion!

- 25.01.2021 Как банкиры 90-х делили «золотую милю» в Юрмале

- 30.12.2020 Накануне 25-летия Балтийский курс/The Baltic Course уходит с рынка деловых СМИ

- 30.12.2020 On the verge of its 25th anniversary, The Baltic Course leaves business media market

- 30.12.2020 Business Education Plus предлагает анонсы бизнес-обучений в январе-феврале 2021 года

- 30.12.2020 Hotels showing strong interest in providing self-isolation service

- 30.12.2020 EU to buy additional 100 mln doses of coronavirus vaccine

- 30.12.2020 ЕС закупит 100 млн. дополнительных доз вакцины Biontech и Pfizer

- 29.12.2020 В Rietumu и в этот раз создали особые праздничные открытки и календари 2021

- 29.12.2020 Latvia to impose curfew, state of emergency to be extended until February 7

«The Baltic Course» Is Sold and Stays in Business!

«The Baltic Course» Is Sold and Stays in Business!