Analytics, Banks, Direct Speech, Education and Science, Financial Services, Interview, Latvia, Shadow economy

International Internet Magazine. Baltic States news & analytics

Thursday, 02.04.2026, 09:18

Economic aspects of anti-money laundering in Latvian banking system

Print version

Print versionJEL codes: G18 – Government Policy and Regulation

|

|---|

| Alexander Masharsky. |

Introduction

Anti-money laundering and counter-terrorism financing (AML/CTF)[1] is one of the key factors of economic, financial, social and political stability of today’s society. The main channel for money laundering and terrorism financing (ML/TF) is banking system.

The establishment and functioning of AML/CTF system on all levels requires substantial expenses, but their evaluation, adequate to the problem of efficient distribution and usage of limited resources, remains not finally resolved.

The available AML/CTF cost-benefit researches in national banking systems are based on different methodologies, analytical methods and procedures that is determined by the shortage and particularities of necessary data and complication of evaluation object.

The topicality of the enhancement of efficiency of anti-money laundering has a special role for Latvia as a regional financial centers, but until now the only AML/CTF cost-benefit valuation has been executed in scope of international research (Transcrime,2006).

An efficient AML/CTF in LBS is impossible without regular related cost-benefit monitoring that requires the determination of approach to the development of CB valuation methodology.

[1] As in 2005 the 3rd Anti-Money Laundering and Counter-Terrorism Financing directive was adopted, both concepts – money laundering and terrorism financing – are considered jointly.

1. Cost-benefit analysis of AML/CTF Activities in Banking Systems

National banking system of AML/CTF is a key element of international and national systems of AML/CTF (Table 1):

Table 1. Organizational System of AML/CTF

|

System levels |

Major system elements |

|

International |

· International AML group (FATF) · Committee of Experts on the Evaluation of Anti-Money Laundering Measures and the Financing of Terrorism 0f Council of Europe (Moneyval) · FATF-style regional groups, including The Eurasian group on combating money laundering and financing of terrorism (EAG) and Wolfsberg Group · World Bank (WB) · International Monetary fund (IMF) · The Egmont Group of Financial Intelligence Units |

|

National |

· Financial Intelligence Departments – Control Service of General Prosecutor of Latvia · Regulation bodies – Finanacial and Capital Market Comission (FCMC), Bank of Latvia etc. · Law enforcement authorities and Court system |

|

Banking |

Internal Control System (ICS) |

Source: The data systemized by the authors.

FATF principles, standards and methodology of valuation of national systems of AML/CTF plays the leading role on international level, but Anti-Money Laundering Law Plyas the leading role on national level.

The main action principle for bank ICS is the principle “Know your client” and “Know the business of your client” that is being realized through the bank AML/CFT strategy, policy, procedures, instructions and measures.

Economic aspect of system operation is determined by economic losses from money laundering and terrorism financing, costs on operation and investments in the development of banking and related government AML/CTF structures, and the characteristics of the system efficiency. The importance of economic evaluation of losses is related to the determination of budgeting priorities by national economy sectors and types of activity for more efficient reduction of ML/TF losses (risk-based approach), but the evaluation of costs and benefits of AML/CTF system operation is related to the development of measures to enhance its efficiency.

As negative consequences on macro level, that cause economic costs and losses, the following should be named:

- A high uncertainty of situation in foreign markets with foreign exchange rates and interest rates that distort market expectations (IMF);

- Obstacles to government tax collection efforts;

- The decrease of potential foreign investments and the efficiency of legal business;

- Large government costs on regulation of banking sectors, financial markets and business environment;

- Costs on financing of necessary information collection and analysis;

- The development and implementation of legalization counter-fighting by regulation and law enforcement authorities in accordance with international recommendations.

The negative circumstances on micro level include:

- The risk of loss of reputation of financial institutions that causes the loss and appreciation of funding sources, but in emergency case – the loss of license;

- Expenses on creation, maintenance and investments in development in banking systems of AML/CTF internal control;

- The loss of a part of clients, financial resources and expenses without sufficient grounds for confidence in their belonging to ML/TF.

The complication of the evaluation of costs and benefits of banks and the government are determined by many factors:

- The variability of aspects and loses of economy where legalization takes place;

- Continuous improvement of schemes and methods of legalization;

- Insufficiency and impreciseness of statistical data;

- The variability of approaches and methods of evaluation.

The researches, carried out in recent years on the base of cost and benefit analysis method (CBA) have shown a high level of costs and a low economic efficiency of regulation and banking AML/CTF systems performance.

For instance, on world level the evaluated benefits from AML/CTF make 0.6% of the world GDP, but the value of ML/TF make 2.7% (1.2 trillion US dollars) (Barone and Masciandaro, 2007).

On regional level, the expenses, related to AML/CTF introduction in Swedish and Norwegian banking systems are evaluated at 400 million SEK and 200 million NOK accordingly (Larsson and Magnusson, 2009).

The costs values on the two options of realization of the principle “know your client” (excluding direct expenses on regulation bodies) is given in Table 2 (PricewaterhouseCoopers, 2003; p.33, p.55.).

Table 2. Costs on the Options of Realization of the Principle “Know Your Client” in the Banks of the United Kingdom

|

Costs on the options of realization of the principles “know your client”, GBP |

А – revealed by the banks |

В – information from clients |

|

Banks for regulations fulfillment, million Per client |

41 2.03 |

16 0.78 |

Source: AML current customer review cost benefit analysis . PricewaterhouseCoopers, 2003.

The analysis of costs and benefits of AML/CTF of Latvian banking system was carried out in 2006 by Italian research centre Transcrime. The data, obtained as the result of investigation of valuation by principle “Know Your Client” realization options are shown in Table 3.

Table 3. CBA by principle “Know Your Client” realization options in Latvian Banks

|

Principle “Know Your Client” realization options, euro |

А – revealed by the banks |

В – information from clients |

|

Cost s, of which direct: Benefits Net benefits |

23,176,000 6,803,000 - - 23,176,000 |

17,490,000 - - - 17,490,000 |

Source: TRANSCRIME, p.164.

http://transcrime.cs.unitn.it/tc/fso/publications/CBA-Study_Final_Report_revised_version.pdf

The results of these researches show the considerable expenditure and low efficiency of regulation and banking system of AML/CTF.

2. Determination of Approaches to the Valuation of Costs and Benefits of AML/CTF in Latvian Banking System

The analysis of conducted researches has shown that in order to evaluate the costs and benefits (CB) of AML/CTF the methods of direct valuation – sociologic researches – and indirect – statistic relations with ML/TF scale – are used, but for the evaluation of the risks (threats) of ML/TF both detailed – sociologic and economic and mathematic modeling-based and generalized – gravitation model of John Walker and expert valuations are applied. (Transcrime,, 2007; Barone and Masciandaro, 2007; Walker and Unger, 2009; PricewaterhouseCoopers, 2003).

Direct valuations, based on sociologic research, where information, collected from all significant and available sources by interrogation (questionnaire) methods, via communication channels and personal contacts, are more precise, but at the same time – substantially more expensive, therefore cannot be used on regular basis.

Since the evaluation of CB of AML/CTF is an equally complicated task, but the CB value depends on the factors of ML/TF value, they should be evaluated, based on general principles.

FATF generalizes the experience of development of national methodologies and guidelines of application of ML/TF valuation methodology in national systems.

The following FATF provisions on the character of ML/TF risks (threats) valuation are of principle importance for methodology development (FATF/OECD, 2008):

· Dependence on valuation objective;

· Impossibility of high preciseness of quantitative valuation;

· The use of qualitative valuation, based on inaccurate data, supplemented with supposition, based on precisely formulated assumptions;

· Taking into account national features;

· System approach to data from different sources and valuations, obtained by different methods.

International valuation of correspondence of AML/CTF system of a country to FATF recommendations that comprises finance and banking system evaluation, is based on FATF expert rating valuation methodology (2004, 2009) and is aimed at stimulation of according institutions to create and enhance the efficiency of AML/CTF. Such valuation is a method of generalized indirect valuation, based on relations with significant variables and indirect indicators and factors.

The main indicators of ML/TF scale in a country are:

· Legal system and regulation norms adequacy to AML/CTF objectives;

· The number of reports on unusual and suspicious transactions, submitted by commercial banks to regulation bodies;

· The number of criminal cases, initiated on the base of the received reports;

· The number of cases, taken to the court and criminated;

· The number of persons brought to responsibility, and the amount of frozen and confiscated money.

The factors of ML/TF scale dynamics are:

· Grey economy scale[1];

· The scale of foreign capital flow through finance and banking system;

The belonging of the country to international financial and offshore centers (geographic profile);

· The character (profile) of bank clients;

· The character (profile) of transactions via banking system.

Therefore, according to generalized indirect valuation the correlation of costs and benefits of AML/CTF with significant indicators and factors will look as follows (Figure 1):

|

|

Figure 1. Correlation of Costs and Benefits with Significant Indicators and Factors According to Generalized Indirect Valuation |

Source: Composed by the authors.

The methodology development, taking into account national features of Latvia, should be based on the total data on significant ML/TF indicators and factors in Latvia. Today the database includes the results of Moneyval and IMF experts’ valuation (2006, 2009), the results of Transcrime researches (2007), and the data of regulation bodies, law enforcement authorities and judicial authorities of Latvia on ML/TF.

According to Moneyval and IMF valuation, in 2006 Latvia met more than a half of FTAF recommendations. Moneyval valuation of 2009 notes further progress. At the same time, it has been mentioned that Latvia still faces a considerable ML threat due to corruption, organized crime and non-residents’ accounts and it should continue to improve its risk-based approach to AML/CTF, to expand information exchange and cooperation between law enforcement authorities, and to enhance the efficiency of legal prosecution and conviction of persons, involved in financial crimes.

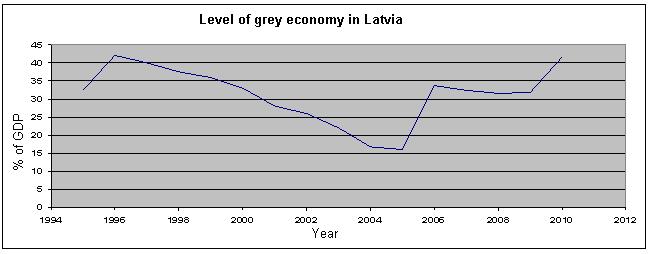

The available valuations of grey economy sector in Latvia in 2010 vary from 11-16% of GDP according to information of Central Statistical Bureau to 39.4% of GDP (Керни, 2008). Domestic economists evaluate grey economy sector level at 20% to 34% of GDP.

For the period from 1994 to 2010 the level of grey economy in Latvia remained practically unchanged (Figure 2).

|

| Figure 2. The Dynamics of Grey Economy Level in Latvia from 1994 to 2010 |

Source: Composed by the authors according to E.Brēķis, “Latvijas ēnu ekonomikas modelēšana nodokļu politikas aspektā”, Rīga, 2007, 36 lpp.

The existing evaluations of government losses from grey economy in 2010 vary from 2.5 billion lats, according to Pēteris Strautiņš, economist of DnB Nord Bank, to 3.6 billion lats according to economist Kerney.

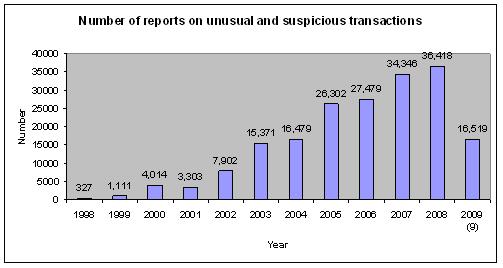

The scale of ML/TF in Latvian banking system is characterized by the following indicators (Figure 3, 4).

|

| Figure 3. Number of Reports on Unusual and Suspicious Transactions |

Source: Composed by the authors according to http://www.vdi.gov.lv/lv/

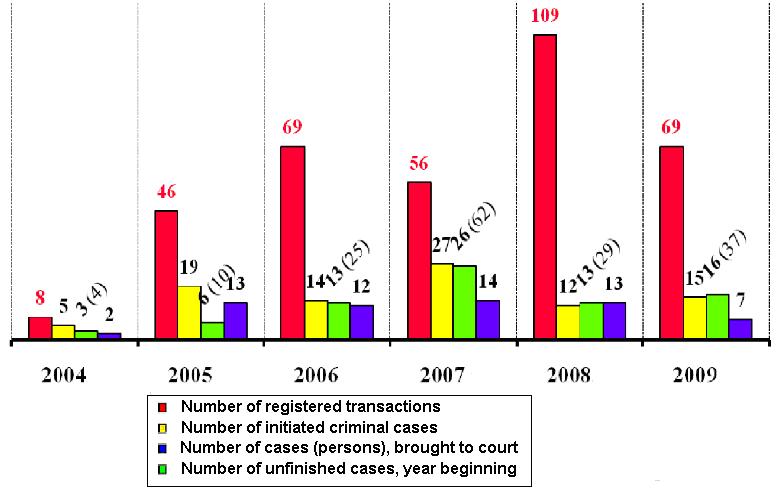

Figure 4 shows the dynamics of results of performance of prosecution in AML/CTF from 2004 to 2009.

|

| Figure 4. The Results of Performance of Prosecution in AML/CTF in 2004-2009. |

Source: Composed by the authors according to www.lrp.gov.lv

As per the results of prosecution, in 2009, 5.2 million lats were frozen and confiscated.

The data of Figure 5 show a sharp increase of the number of reported unusual and suspicious transactions to Control Service of General Prosecutor of Latvia. At the same time, the number of initiated and brought to court cases does not correlate with the dynamics of reports. According to the records of Control Service, most of reports were formal and after consultations with the banks, organized in 2008, the number of reports decreased. Besides a more conceptual approach to the evaluation of reports, economic downturn in the country that caused the decrease of the number of transactions also played its role.

It can be supposed the divergence between the dynamics of grey economy sector (Figure 2) and the number of reports (Figure 3) can be explained with the transition of transactions from non-cash settlements to cash circulation.

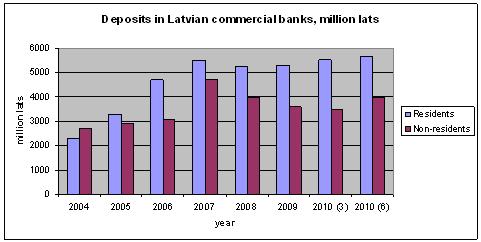

It is especially important for Latvia to analyze the value and dynamics of non-residents’ deposits and transactions (Figure 5). In 2008, 71% of total non-residents’ deposits in the Baltic countries were put to Latvian banks.

As Figure 5 shows, starting from 2008 there is a trend of decrease of non-residents’ deposits in Latvian banks that was caused not only by the adoption of 3rd EC Directive, but also the loss of trust to Latvian banking system overall. In 2008 a part of non-residents’ deposits was transferred to Cyprus, but in 2010 a part of them was returned back due to economic downturn in Greece.

Such facts like large-scale transactions in US dollars coming from the East; large portion of non-residents’ deposits in Latvian banks, the cease of VEF banka activity and problems of Multibanka as the result of the requirements of US Treasury (2005), the withdrawal of Ogres komercbanka license (2006); recent referral of General Prosecutor of Kazakhstan in connection with the transfer of stolen money of “BTA Bank” to off-shores through commercial banks of Latvia are the evidence of continuous use of Latvian banking system for money laundering. Therefore, despite the positive dynamics of several indicators and favorable valuations of Moneyval and IMF, the costs and losses from ML/TF cannon be insignificant both for national economy overall and for Latvian banking system.

|

|

Figure 5. The Dynamics and Portion of Non-residents’ Deposits in Latvian Banks |

Source: http://diena.lv/lat/business/hotnews/finance/eksperts_dati_par_nerezidentu_noguldiijumiem_buutiski_kontekstaa_ar_finanshu_pakalpojumu_eksportu:

An important step in enhancement of AML/CTF efficiency in Latvian banking system should be systematic investigation of costs and benefits of AML/CTF, based on valuation methodology, taking into account national features of Latvia.

It is expedient to make such analysis, combining both direct and indirect methods; thereby a more precise and labor-intensive analysis should be carried out in case of necessity, but the less precise indirect analysis should be made on regular basis. The specifics of LBS should be reflected as the content and significance level of indicators and factors of foreign capital flow through LBS from the East.

In the authors’ opinion, the preciseness to cost ratio of regular valuation could be improved by supplementing expert valuation option of indirect valuation method with correlation-regression model of statistical relation of quantitative values of CB, obtained as the result of direct valuation, with the indicators and factors of ML/TF. The values of correlation coefficients should be précised when making direct valuations.

The initiation of discussion of necessity and organization of the development of methodology of valuation of costs and benefits of AML/CTF in cooperation with Finanacial and Capital Market Comission and Association of Latvian Commercial Banks is the competence of Financial Sector Development council of the Cabinet of Ministers of Latvia.

[1] Grey economy scale evaluation is an analogous complexity task and there are more than dozen various methods used to solve it.

Conclusion

· Anti-money laundering and counter-terrorism financing (AML/CTF) os one of the key factors of stability of today’s society, but banking system is the main channel of ML/TF.

· The importance of enhancement of AML/CTF efficiency has a special meaning for Latvia as a regional financial center.

· The results of foreign researches show the high costs and low efficiency of regulation and banking system of AML/CTF.

· The existing AML/CTF cost-benefit valuations in national banking systems are based on different methodologies, analytical methods and procedures that impedes comparative analysis and aggregated valuations by regions.

· The generality (invariance) of the character and correlations of СВ and МL systems are the evidence of the possibility of usage of the principles of development of national methodologies of ML risk valuations, included in FATF recommendations, for the development of national methodologies of AML/CTF СВ valuation.

· According to these principles, the development of FATF methodology of valuation of ML/CTF for cost-benefit valuations should be based on complex usage of various valuation methods – both direct and indirect evaluation methods; both statistic models and expert valuations, taking into account national features and a total of significant indicators and factors of ML/TF in Latvia.

· The specifics of LBS should be reflected as the content and significance level of indicators and factors of foreign capital flow through LBS from the East.

· The advanced approach would be the use of valuations, obtained as the result of both direct and indirect methods with the use of correlation-regression analysis of statistical relation of quantitative values of costs and benefits, obtained as the result of direct valuation, with ML indicators and factors.

· Today AML/CTF in Latvian banking system has rather favorable Moneyval and IMF valuations; however, AML/CTF still remains a serious problem, but losses from ML/TF remain significant both for economy overall and for Latvian banking system.

· A systemic research of AML/CTF cost-benefit valuations, based on valuation methodology that takes into account national features of Latvia, would enhance AML/CTF efficiency in Latvian banking system.

References:

1. AML Current Customer Review Cost Benefit Analysis, Prepared by PricewaterhouseCoopers LLP 23 May 2003. http://www.fsa.gov.uk/pubs/other/ml_cost-benefit.pdf

2. Barone Raffaella, Masciandaro Donato . Worldwide anti-money laundering regulation: estimating the costs and benefits .16 .08.2007

3. Brēķis E. Latvijas ēnu ekonomikas modelēšana nodokļu politikas aspektā. – Rīga, 2007. – 36 lpp.

4. Committee of experts on the evaluation of AML/ FT , MONEYVAL(2009)

5. Cost Benefit Analysis of Transparency Requirements in the Company/Corporate Field and Banking Sektor Relevant for the Fight Anti Money Laundering and Other Financial Crime. Final Report. TRANSCRIME, 27.02.07. http://transcrime.cs.unitn.it/tc/fso/publications/CBA-Study_Final_Report_revised_version.pdf Directive 2005/60/EC of the Europien Parlament and of the Council of 26 October 2005 on the prevention of the use of the financial system for the purpose of money laundering and terrorist financing. // http://eur-lex.europa.eu/LexUriServ.do?uri=OJ:L:2005:309:0015:0036:EN:PDF6. Hans Geiger and Oliver Wuensch, The Fight Against Money Laundering –An Economic Analysis of a Cost-Benefit Paradoxon _, September 2006, Swiss Banking Institute, University of Zurich . http://www.hansgeiger.ch/files/060929_AmlEconomicAnalysis.pdf

7. KMPG study Global Anti-Money Laundering Survey 2007., 15-45.lpp.

8. Larsson Paul, Magnusson Dan. The Cost of ML Regulation/ Summaries fra 96. Argang Nr.1-April 2009

9. Latvia Progress report 9.12. 2009 (Second 3rd Round Written Progress Report Submitted to MONEYVAL)

10. LR Likums “Par noziedzīgi iegūtu līdzekļu legalizācijas un terorisma finasēšanas novēršanu”. / Latvijas Republikas likums. Pieņemts Latvijas Republikas Saeimā 17.07.2008.; stājies spēkā 13.08.2008.; // Latvijas Vēstnesis, 30.07.2008., Nr.116 (3900)

11. Methodology for Assessing Compliance with the FATF 40 Recommendations and FATF 9 Special Recommendations 27.02.200412. Novicka A. Eksperts: Dati par nerezidentu noguldījumiem būtiski kontekstā ar finanšu pakalpojumu eksportu. // http://diena.lv/lat/business/hotnews/finance/eksperts_dati_par_nerezidentu_noguldiijumiem_buutiski_kontekstaa_ar_finanshu_pakalpojumu_eksportu

13. Prosecutor of the Republic of Latvia. // www.lrp.gov.lv

14. State Labor Inspection Homepage. // http://www.vdi.gov.lv/lv/

15. Third Round Detailed Assessment Report on Latvia: Anti-Money Laundering and Combating the Financing of Terrorism, June 2007

16. United States Department of State Bureau for International Narcotics and Law Enforcement Affairs International Narcotics Control Strategy Report Volume II Money Laundering and Financial Crimes March 2009

17. VID vadītāja ēnu ekonomiku Latvijā „samazina” uz pusi. // http://www.kasjauns.lv/lv/zinas/13728/vid-vaditaja-enu-ekonomiku-latvija-samazina-uz-pusi

18. Walker John and Unger Brigitte (2009) "Measuring Global Money Laundering: "The Walker Gravity Model"," Review of Law & Economics: Vol. 5:Iss. 2, Article 2. http://www .bepress.com/rle/vol5/iss2/art2.

19. Zemāki nodokļi – mazāka ēnu ekonomika. // http://scenariji.lv/2010/08/zemaki-nodokli-%e2%80%93-mazaka-enu-ekonomika/

20. В Латвии отмывают деньги. // http://rus.tvnet.lv/novosti/ekonomika/151959-v_latvii_otmivajut_djengi, 5.09.10.

21. Группа разработки финансовых мер по борьбе с легализацией денежных средств, полученных преступным путем. Справочный документ ФАТФ. Неофициальный перевод. Оценки, осуществляемые в рамках ПОД/ФТ. Пособие для стран и экспертов. Апрель 2009 г

22. Стратегии оценки рисков легализации денежных средств, полученных преступным путем, и финансирования терроризма. Неофициальный перевод. ФАТФ/ОЭСР, 2008 http://eurasiangroup.org/ru/news/typ_strat.pdf

«The Baltic Course» Is Sold and Stays in Business!

«The Baltic Course» Is Sold and Stays in Business!