Analytics, Baltic, Banks, Financial Services, Society

International Internet Magazine. Baltic States news & analytics

Sunday, 05.04.2026, 06:38

Despite the bankruptcy of Snoras and Krajbanka, satisfaction of Baltic banking clients didn’t change in 2012

Print version

Print version

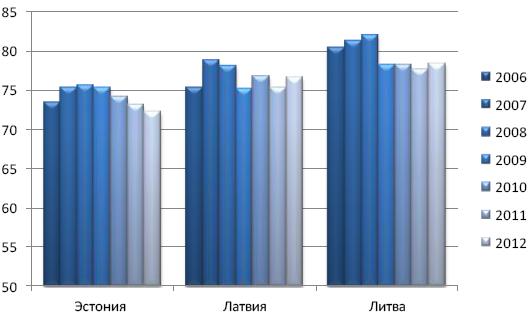

Satisfaction of

Lithuanian customers is highest as it was also during the previous years (78.4

points out of 100), followed by Latvian (76.7) and Estonian (72.3) customers

evaluations. Considering the satisfaction of all respondents, we may see only

slight changes in evaluations in comparison to previous year: less than 1 point

difference on the 100 point scale. However, the evaluations for different banks

separately are not so homogenous.

|

| Satisfaction index, banking B2C sector by country, 2006-2012 |

Satisfaction

In Estonia the evaluations of satisfaction with individual banks varies between 67 points put of possible 100 for Sampo and 74.2 points for Swedbank. In comparison to the results of 2011, evaluations for Sampo (-6.3) and SEB (-2.5) decreased substantially, while other banks experienced only slight changes. Moreover, evaluations of Nordea and Swedbank have some positive drift. The most satisfied are customers of Swedbank, followed by customers of smaller and niche banks. The evaluations of Nordea customers are rather steady, but small positive change together with drop in evaluations of SEB and Sampo, moved Nordea in customer satisfaction ranks from last to third place this year. Same time, last year top performers SEB and Sampo got the lowest evaluations this year.

Satisfaction index, banking B2C Estonia, 2011-2012 and change

In Latvia the satisfaction scores this year are between 71.5 (Citadele) and 79.4 (DNB). Evaluations for all the banks measured individually increased to some extent. The highest increase is for Swedbank (+3.7 points), which could be to some extent an affect of “Brainstorm” concert organised by the bank for its clients in August, when the interviewing of respondents also took place. The second highest increase is for DNB (+3). The results for Citadele, which administrated the payback of deposits of failed Krajbanka, also increased (+2). Overall, DNB took a confident first position, while Swedbank and SEB share the second place in customer satisfaction.

Satisfaction index, banking B2C Latvia, 2011-2012 and change

Satisfaction of banking customers in Lithuania varies between 77.4 (other) and 80.1 (Swedbank) this year, becoming even closer to each other leading to tighter competitions between banks. SEB and Swedbank experienced the growth in their evaluations which could be related to the fact that these banks, especially SEB, overtook the major share of clients of failed Snoras bank. The evaluations of DNB clients stayed on same level as last year, while the results for group of other banks slightly decreased. The decline appeared because results for Nordea bank were included this year under the group “other”, not presented separately as it has been before.

Satisfaction index, banking B2C Lithuania, 2011-2012 and change

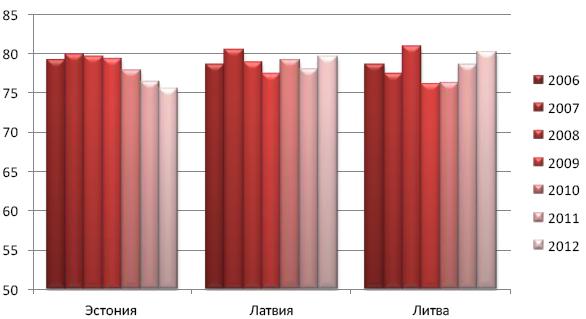

Loyalty

Another important

issue to look at is the loyalty of the customers. According to the EPSI Baltic

study 2012, slight positive changes took place in Latvia and Lithuania (+1.6

point each), while evaluations for Estonia continue to follow the negative

trend.

|

| Loyalty, banking B2C sector by country, 2006-2012 |

In Estonia, customers are most loyal to the group of “other” banks, as also last year, probably because this group consist of various smaller banks operating in their niche and customers choose these banks because of some specific reason. The willingness to stay with the bank or to recommend it to others was evaluated close by the customers of Swedbank (76.7) and SEB (75.5), while the results for Sampo (65.9) decreased dramatically. The only bank whose customers loyalty increased this year is Nordea (78.1).

In Latvia, clients of DNB (82.6) and Swedbank (81.5) are the ones willing to stay with their banks. Evaluations for Nordea (79.2) increased, catching up with the high level of SEB (79.4 points), while clients of Citadele (69.3) still hesitate. Their evaluations increased significantly, but the level of evaluation in comparison to other banks is still relatively low.

The situation in Lithuania is similar to Latvia: loyalty scores are also highest for Swedbank (82.6) and DNB (80.7), followed by SEB (79.3) and other (78.6). Overall, loyalty of all Lithuanian customers to their banks is on the same high level with only 4 points range.

What influences customers’ satisfaction and loyalty?

These are various aspects, presented in EPSI questionnaire in about 40 different questions. The evaluations of these questions are grouped under 5 topics or indices: Image (how, according to the respondent, society overall would rate some aspect of their bank), Expectations (what customers expected to get from the bank based on their experience), Product and Service quality (what respondents actually get in terms of banking products and services), Value-for-money (if, according to respondents, the charges are reasonable for the quality of products and services they get). The results for three out of five mentioned indices are presented in the next section.

Estonia

The greatest negative drop appeared in evaluations of Sampo bank, especially value-for-money aspect. The customers of Sampo bank consider that they pay too much for the kind of products and services they get.

· Unfortunately, also SEB was evaluated worse than in 2011 in majority of aspects with the exception of Service quality. On the example of this bank it is obvious, that service quality is not always the main thing for clients’ satisfaction.

· Biggest positive changes are for Nordea, which service and product quality is evaluated higher than in 2011.

· Also evaluations of services of the group of smaller banks increased.

Latvia

Changes in evaluations in Latvia are much smaller than in Estonia for majority of the banks.

· The highest positive changes could be seen in evaluations of SEB in all three aspects presented here: service and product quality and value-for-money.

· Swedbank clients also evaluated service quality and value-for-money higher than a year ago.

· The change in evaluations for DNB are rather small in comparison with 2011, but this bank received highest evaluations from its customers in 2012 in all aspects in comparison to other banks in Latvia.

Lithuania

Positive changes may be seen for product quality of Swedbank, as also value-for-money evaluations

· Product quality evaluations increased substantially also for SEB

· Evaluations of all aspect decreased for smaller banks. As also mentioned before, the main reason for that is since evaluations for Nordea bank are included under this category this year and not presented separately.

· Overall, evaluations of all aspects for all banks are very close this year with no distinctive leader, especially in product quality. DNB is leading in service quality, while Swedbank value-for-money results are the highest.

These are extracts of the EPSI Baltic Customer Satisfaction Study conducted in 2012 among the banks’ private and corporate consumers in three Baltic countries. Industry averages are calculated based on results for individual banks and their respective market shares. The results for banks having high market share (usually more than 8%) are presented separately, while results for smaller banks are given together under “other” banks group.

The study has been done as an integral part of the Extended Performance Satisfaction Initiative (EPSI Rating). Thus, the results can be compared with those available on an annual basis from many other countries (some benchmark can be found in the end of this press release). The study is done in order to support the development of customer oriented and driven services throughout Europe.

The study is based on interviews with around 5 000 individual and corporate customers representing all three Baltic States. The data collection company Norstat conducted it over the telephone. Each person or company representative was interviewed about one specific bank which she/he uses most often.

_________________________________________________________________

* Customer Satisfaction measure is leading not-financial indicator capturing crucial information about future trends and market development. There is also a strong positive relationship between customer Satisfaction –> customer Loyalty –> company Profitability.

The satisfaction index is reported on the scale 0 – 100. The higher score – the more satisfied customers. Averages usually fall in the region 70-75 for Latvia, 65-75 for Estonia and 75-85 for Lithuania. Any company receiving a score above 80 has a strong position among its customers, while those below 65 face risks of losing the customer base. The statistical precision is good for the overall results, and a difference of 2-3 units or more for the country average is statistically significant.

«The Baltic Course» Is Sold and Stays in Business!

«The Baltic Course» Is Sold and Stays in Business!