Analytics, Economics, Employment, Financial Services, Foreign trade , Inflation, Latvia

International Internet Magazine. Baltic States news & analytics

Sunday, 21.06.2026, 08:01

Commercial Banks' Association presented Latvia’s Economic Outlook 2009

Print version

Print version |

|---|

It is important to note that Latvia’s image in the eyes of the creditors and investors is slowly improving. All the necessary decisions, no matter how unpopular economically and socially they are, have been adopted and the economy is showing some signs of recovery. Very drastic cut of labour costs in the private sector has helped improve competitiveness and in several areas increase the market shares in the main export markets. Unfortunately, our previously expressed concerns of the delayed and controversial activities of the policy makers and implementers have come true. Restructuring of the state administration and the public sector is too slow, improvements of the business environment are overdue, and changes in the tax policy have been fragmentary, badly advertised and sometimes even harmful for competitiveness while utilisation of the EU structural funds takes too much time.

The steepest fall is over

In the 3rd quarter Latvia’s economy followed the same trend as before and GDP dropped by 19%. Despite the growing export volumes, the GDP fell so low due to the sharp reductions in household incomes, weak investment activity and decreasing public spending. Household consumption and investments into the share capital, compared with 2008 fell by 28% and 39% respectively, yet the downward trend was not so steep any more. The low utilisation of capacities leads to the conclusion that in the near future the investments will still remain very low. Spending will be equally weak as the household incomes keep shrinking and the state budget will require stricter consolidation in order to make it sustainable.

These trends are visible in the industries where the sectors oriented to local consumption are still in deep freeze (construction –36%, hotels and restaurants –31%, trade –28.7%, individual services –20%). Quite impressive cargo volumes in the ports and on the railway have not managed to offset the overall decline in the transport and communications sector (-18.2%). A big fall was observed in public sector spending where saving measures and job cuts in Q3 were substantial. Still, untypical immunity to the crisis is observed in Latvia’s biggest sector, – commercial services – in which real estate and rent operations bring in the biggest contribution.

For a couple of quarters some confusingly little negative figures were seen, whereas in Q3 a small growth appeared, which looks more like a single leap or even more probably, a statistical error rather than the change of the trend.

As expected, the situation started to improve in industry, which is associated with the greatest hopes with regards to overcoming the crisis. Manufacturing is increasingly supported by the foreign markets that are beginning to open and, thanks to the improved competitiveness of many enterprises, encourage forecasts of considerably better results already after a few quarters of the year. Although in Q3 in annual terms there was a two-digit fall, in comparison with Q2 there already was a small rise both in terms of volumes and value.

Compared with the previous quarter, the positive developments were observed in textile, wood, paper, metal, computer, electronic equipment and furniture industries.

In the quarters to come the number of industries with positive results will keep growing. Most probably in 2010, in annual terms, the majority of industries will show growth. Generally, we can conclude that the sharpest decline in economy is already behind us. It is also clear that more brisk utilisation of the EU structural funds and more significant improvements in the business environment as well as faster and more effective reform of the public administration would have contributed to even better results in Q3. The downturn of the economy in the last quarter of 2009 remained quite sharp, yet it will

subside at the beginning of 2010. The second half of the year could already see some slight improvement. The economy is expected to reach the lowest level of activity in the middle of 2010. The data can be significantly affected by the businesses entering the gray economy zone, the irresoluteness, doubts, lack of stable positive signals and protectionism trends that are increasingly noticeable in the Russian market.

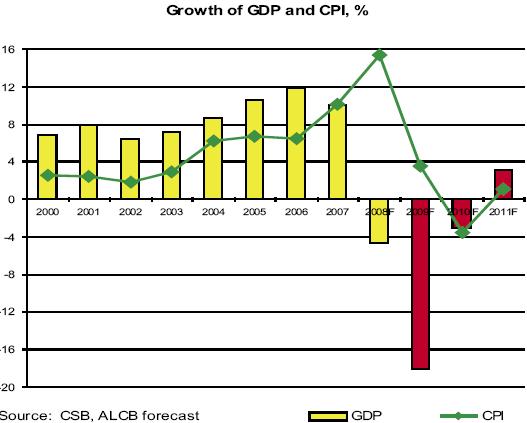

ALCB retains its summer forecast of an 18% fall in the economy for 2009 as the processes in the economy have developed according to the scenario outlined by us. In 2010 GDP will decrease by 3%, whereas for 2011 we predict growth of 3.2%.

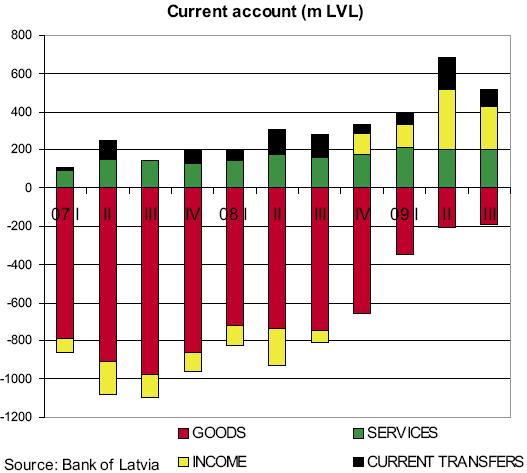

Positive changes in the balance of payments

In a very short period of a few quarters an unexpectedly fast improvement was observed in Latvia’s balance of payments where over several years the effects of economic imbalances and reluctance to address them politically and administratively had been accumulating.

It is one of the best examples of flexibility of a small and open economy. This very positive example is pointed out by the international creditors and credit rating agencies and it must be viewed as one of the decisive factors in Latvia’s progress towards sustainable development.

If still in the first 3 quarters of last year the current payment account deficit was 15.4% of GDP, this year in the same period there was surplus of 8.6% of GDP. Besides, in Q2 surplus was 14.1%, and in Q3 it was 10.1%.

Such spectacular changes over so short a period of time cannot be found in the global history! Latvia is slowly learning to live within its income rather than on borrowed money. Domestic spending has shrunk considerably while exports of goods and services are gradually improving. Imports of goods in 10 months fell by 42%, while exports were down by 25%, thus reducing the negative foreign trade balance almost threefold. From the improvement of the industrial data we can conclude that already next year exports will show positive results in annual terms. It is very important to note that even during the downturn of the global economy we have managed to keep exports of services stable generated mostly by the transit flow through the Latvian ports.

For two quarters already the positive balance of services has offset the negative balance of goods, which is crucial for sustainable economic development. The situation will roughly remain the same in the coming couple of years although the current account surplus will slowly shrink as the economy begins to recover.

It will also happen due to the fact that the big current surplus is created by the losses of commercial banks showed as the positive balance of the income account. These are expected to significantly decrease next year together with the overall current account surplus.

Notably, although overdue loan payments in the banking sector continue to increase, the rate of provisions (9.3% as at end of November) has slowed down considerably compared with the first half of 2009. The banks keep restructuring their loan portfolios and increase their capital. Clearly, the commercial banking sector of Latvia has proved its ability to sustain the economic downturn even considering the fact that the total volume of the loan portfolio still exceeds the country’s GDP. Although the banks are urged to distribute credits more freely in order to impact the economy, it will not happen until significant improvements in the sovereign credit rating, the financial results of companies and households and the state support to the business activity are achieved.

Road of deflation

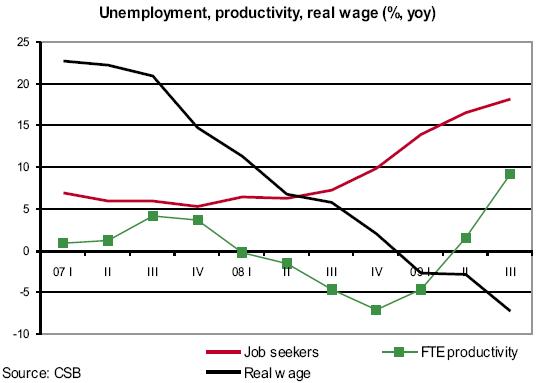

Deep correction has taken place in the labour market. According to the CSB data the wage and salary fund (i.e. the income of the employed population for consumption) from the end of 2008 till Q3 of 2009 decreased by 30%. Employment in full-time work units in the same period dropped by 23%, due to considerable decline in the number of the employed and the hours spent at work. Year on year, the labour cost per unit in Q3 decreased by 13.5%, and that was the second consecutive quarter when Latvia’s competitiveness improved.

Nevertheless, it does not mean that the homework has been accomplished. Improvement in competitiveness is not sufficient yet and so far it has been gained to a large extent by job cuts and/or reduction of working hours.

Such a strategy cannot be pursued endlessly, and for the competitiveness to become sustainable, it must become „wiser.” If the public sector reforms and improvement of the business environment are delayed, productivity will rise slowly leaving the burden of competitiveness on the shoulders of employment and wages and salaries. Given that the ratio of jobseekers in December already reached 16%, the correction in the private sector will mostly take place at the expense of wage cuts while in the public sector there is still potential for reduction of vacancies. If reduction of labour costs is necessary at the initial stage of correction because of the soaring wages and salaries in the fat years, now there is a critical need for structural reforms to take the pressure off the labour market, reduce the social tension and preserve the future growth resource that can be depleted by mass emigration.

Although the business people often blame the government and politicians, healthy self-criticism, constructive proposals, consolidation and focussed joint progress to sustainable economic development are very crucial indeed.

The correction of the labour market has been immediately reflected in the consumer prices which since October show deflation expected to continue in 2010 and reach into the year 2011. The weaker the progress of structural reforms, the deeper the fall in household incomes and hence the harder pressure of deflation. This in its turn will reduce the ability of the households and companies to service their debts and will curb the increase of consumption and investments. The negative effects of deflation could be minimised by efficient bankruptcy procedure.

It was crucial to adopt the budget for 2010 with total consolidation of LVL 500 million or 5% of GDP. Sadly, not all the implemented consolidation measures have been successful. In our opinion a bigger tax should be levied on the dwelling space, which would decrease the regressive character of the existing tax system that puts a bigger tax burden on the residents with lower incomes.

Besides, it would have been easier to administrate. Increase of the residents’ income tax from 23% to 26% is short-sighted, because it is a complicated tax for administration and enhances the shadow economy. In the tax system it is necessary to continue the reforms in order to minimise its regressive character, negative effect on the companies’ competitiveness and to improve administration.

The increase in the budget expenditure by almost LVL 200 million at the end of the year shows that fiscal discipline also must be improved. The decision of the Constitutional Court on the unlawfulness of the pension cuts in July 2009 means that prior to signing documents with the foreign creditors the government will have to find the resources for budget consolidation by additional LVL 100 million. In our opinion, they could be raised by continuing the structural reforms (e.g. in public administration, education), more effective tax collection and substantial improvement of the government’s dialogue with the public. Further raising of taxes is not a good idea – attention should be paid to shifting of the tax burden and minimisation oft he shadow economy.

What shoul be done?

Reacting to short-term challenges to adopt decisions with long-term perspective. It would be the greatest mistake to give in and leave the reforms of public sector efficiency and improvement of business environment half-finished, as it would essentially slow down future growth and threaten with stagnation, emigration and social tension.

By carrying out structural reforms in the public sector to focus on the quality of public services and pay close attention to addressing of the most serious problems (e.g. higher education, health service).

It is necessary to elaborate tax policy reforms quickly and finally in order to minimise their regressive character and effect on the competitiveness of businesses as well as to improve their administration. The result must be clearly communicated in order to minimise the uncertainty for the business community.

As a priority of the national importance to set stabilisation of the sovereign credit rating with positive outlook that would give encouragement to the economy, improve the investment climate in Latvia, our entrepreneurs’ operations outside the country, and gradually renew crediting.

Enhancement of crediting should be viewed in context with the sovereign credit rating, the insolvency process, trade insurance and other related factors. To continue focussed and effective improvement of the business environment by setting measurable targets and continuously monitoring them, and informing the public of the results.

ALCB considers it important and calls for the following actions:

* By reacting to short-term challenges to adopt decisions with long-term perspective. It would be the greatest mistake to give in and leave the reforms of public sector efficiency and improvement of business environment half-finished, as it would essentially slow down future growth and threaten with stagnation, emigration and social tension.

* By carrying out structural reforms in the public sector to focus on the quality of public services and pay close attention to addressing of the most serious problems (e.g. higher education, health service).

* It is necessary to elaborate tax policy reforms quickly and finally in order to minimise their regressive character and effect on the competitiveness of businesses as well as to improve their administration. The result must be clearly communicated in order to minimise the uncertainty for the business community.

* As a priority of the national importance to set stabilisation of the sovereign credit rating with positive outlook that would give encouragement to the economy, improve the investment climate in Latvia, our entrepreneurs’ operations outside the country, and gradually renew crediting.

* Enhancement of crediting should be viewed in context with the sovereign credit rating, the insolvency process, trade insurance and other related factors.

* To continue focussed and effective improvement of the business environment by setting measurable targets and continuously monitoring them, and informing the public of the results.

ALCB forecasts

|

|

2008 |

2009(p) |

2010(p) |

2011(p)

|

|

GDP, % |

-4.6 |

-18.0 |

-3.0 |

3.2 |

|

Inflation (CPI), % |

15.4 |

3.6 |

-3.5 |

1.1 |

|

Adjusted unemployment level, % |

7.5 |

18.0 |

21.0 |

15.5 |

|

Net wage trend, % |

22.5 |

-4.8 |

-9.0 |

2.0 |

|

Current account balance, % of GDP |

-12.6 |

9.4 |

6.0 |

3.0 |

|

Fiscal balance, % of GDP |

-4.0 |

-9.3 |

-8.0 |

-5.5 |

«The Baltic Course» Is Sold and Stays in Business!

«The Baltic Course» Is Sold and Stays in Business!