Analytics, Baltic States – CIS, Banks, EU – Baltic States, Financial Services, Forum, Latvia, Round Table

International Internet Magazine. Baltic States news & analytics

Tuesday, 09.06.2026, 06:43

The EU measures to manage the financial sector: expected effects for banks

Print version

Print versionThe article is prepared for the Round Table “Baltic States' bank sector: lessons from the modern crisis”, organised by the Baltic International Academy, Latvian Employers Association and International Web-Magazine “The Baltic Course” on 24st of February in Riga, Latvia.

|

|---|

| Eugene Eteris. |

The negative effect of financial institutions on economies was felt in all EU member states and in both private and public sectors. First public reaction was to bailout the falling banks: e.g. in the Baltics, with the most vivid example of privatized Parex Bank, though examples are numerous in other EU states as well on another side of the Atlantic. When the financial crisis went deeper into the economic spheres and “returned” in full swing into the public sector (in the period’s beginning at the end of 2008- start of 2009) only big and powerful states could afford “saving” the banks. In 2009 most of the EU members adopted new “salvation” economic policies, however, the loss of national wealth caused by the measures to alleviate the crisis made some EU states particularly exposed to negative outcomes for employment and public spending.

These measures will have to take time to be assessed and implemented in the member states. So far, numerous states experience great after-chock effect when “real bank’s influence” on economic development is felt in the beginning of 2010, e.g. in Greece.

Main lesson from the financial crisis was that national supervisory structures were insufficient to supervise internationally active banks; hence the need for powers to regulate cross-border banks in line with the European level effective oversight.

First steps

After the signs of full-blown crisis swept European states, the EU institutions’ first reaction was through Council’s actions. Member states’ ministers of economy and finances made some recommendations in October 2008 that their agreed to follow; these recommendations, turned into so-called “common position”, are well worth remembering:

- Interventions should be timely and the support should in principle be temporary;

- The member states will be watchful regarding the interests of taxpayers;

- Existing shareholders should bear the due consequences of the intervention;

- The governments should be in a position to bring about a change of bank’s management;

- The banks and financial institutions’ management should not retain undue benefits, i.e. governments may have inter alia the power to intervene in remuneration (banks’ bonus culture can be described as “heads I win, tails you lose”);

- Legitimate interest of competitors must be protected, in particular through the state aids rules;

- Negative spill over effects should be avoided.

This Council’s “common position” is still valid for the member states.

EU financial regulation: historic overview

October 2008: European Commission asks former French central banker Jacques de Larosière to advice on overhaul of financial supervision in Europe, and prepare a comprehensive report.

February 2009: De Larosière report recommends improvements including a new “systemic risk” board at the macro-level, and new European supervisory agencies, each for banking, insurance and securities markets at the micro-level.

March 2009: De Larosière gets broad endorsement but some countries, including the UK, express reservations. Some worries appeared about possible split of fiscal responsibility from supervisory responsibility.

May 2009: European Commission details plans for implementing the proposals; it suggested installing a new financial supervision system in place in 2010.

June 2009: EU finance ministers give outline approval but with caveats on fiscal responsibility and binding mediation. EU leaders follow suit.

September 2009: European Commission unveils draft legislation to implement the changes. The board will have no direct powers, but will meet regularly and report to EU finance ministers and leaders.

January-February 2010: New and “old” rescue instruments for Greece and other Mediterranean countries in critical conditions are installed.

The European Union’s approach to financial and economic regulations

The way the EU institutions and the member states have responded to the financial and economic stresses the need for common strategies that would promote European principles and long-term economic goals. From the crisis’ start in 2008, the EU played an important role in coordinating the member states’ positions.

Through concerted action, the EU has succeeded in preventing a collapse of the European financial markets and economies, in sustaining growth, though at a meager pace.

The EU-27 is presently implementing Union’s economic recovery plan that represents the most ambitious and solid effort ever taken to coordinate member states’ economic policies; the plan seeks to strengthen the single market, sustain economic growth while attempting to reject protectionism.

The EU recovery plane represents a complex approach to regional economy and finances.

Analysing main documents adopted by the EU institutions during 2008-2010, the following major instruments and policies to manage the economic and financial downturn have to be underlined:

1. Measures to support economy. The EU’s efforts on reviving growth, building stronger and more stable economy underline the importance of coordinated national policies. At the core of it are combined efforts to give the economy a solid boost through investments: the EU has committed roughly ÿ 400 bn (initially about 3,3 per cent of EU-27 GDP, which was later increased to 5 per cent over two years) to stimulate business activity. Though the full impact of stimulus is not yet clear, the recovery will be gradual presenting new economic challenges, e.g. transition to a low-carbon economy, diversification of energy sources, promoting leading-edge industries and innovations. Small and medium enterprises are receiving special attention through Small Business Act, adopted in 2008.

2. Measures to support employment. The crisis is expected to shed about 3,5 mln jobs; the situation calls for a major mobilisation of human resources, creating and protecting jobs. The EU intends to spend about ÿ 1,8 bn in social fund payments during coming years to support millions of workers. The Commission has expanded the scope of funding to help workers hit by shifts in world trade (the new rules lower the amount of matching funds required from member states). A special fund was created for this purpose, so-called Global Adjustment Fund.

3. Measures to reform financial system. In March 2009, the Commission proposed two new instruments: European Systemic Risk Council (ESRC) to provide an early warning of system-wide risks and issue recommendations for action to deal with these risks; and European System of Financial Supervisors, ESFS to safeguard financial soundness at the level of individual financial firms and protect consumers of financial services (“micro-prudential supervision”).

This network is based on the principles of partnership, flexibility and subsidiarity.

Some other issues are involved in the cross-sectoral approach to economy and finances:

- the EU authorities are more inclined to elaborate new approaches to economics, as a science section providing “rules” for economic development, both at macro- and micro-economic level;

- the EU-2020 strategy forming a perspective for a new decade and formulating main directions in member states’ economic and financial cooperation.

The European Commission unveiled on 23 September 2009 draft legislation aimed at providing safeguards against a repeat of the financial crisis that started in 2008. This step signifies a radical reshaping of Europe’s financial supervision system. The new system of mentioned two institutions (ESRC and ESFS) is aimed at streamlining financial sector in the EU and the Baltic States as well.

Thus, a more centralised system of financial supervision is being established in Europe. The Commission revealed its plans to assess and abolish the threats to financial stability in Europe. A new body made up of central bank governors for all the EU-27 member states, chaired by the president of the European Central Bank, which will also provide working support.

Separately, there will be a new European System of Financial Supervisors, which will oversee individual banks and financial firms. Its role will be to develop harmonised rules and common approaches to supervision.

Two new financial watchdogs: pros & cons

Europe’s two new financial supervisory watchdogs are established to oversee systemic risks and watch over individual financial institutions. Governor of the Bank of England since 1991, Mervyn King is appointed the deputy chairman of the European Systemic Risk Board, which will monitor financial stability (the nomination acknowledged the importance of the British financial sector in Europe and the world).

Another new watchdog’s institution is the European System of Financial Supervisors (with an annual budget of € 68 mln; the UK financial regulator spends £ 323 mln a year, and the US regulator almost $1bn). The biggest concern is the balance of power between the ESFS and the financial regulators in the member states. The intention in the EU authorities is to provide for a “single rule book” in case of disagreement among the national financial regulators.

These rules raised immediate concerns in some EU member states, first of all, over the extent to which the new pan-European financial authorities would help enforce common rulebooks within the 3 interrelated financial markets: banking, insurance and securities.

European Commission acknowledged that the new rules would prohibit new financial authorities from taking decisions that could impinge on the member states’ “fiscal responsibilities”. Instead, as an additional safeguard, any EU member state could appeal to the Commission if she believes that this principle had been breached.

Commission envisaged both fierce debate on the proposals’ inauguration and the need for support from both member states and the European Parliament. In some countries, the proposed overhaul was viewed as a first step to closer integration of financial services supervision. This opinion was endorsed by both Charlie McCreevy, the EU internal market’s commissioner (2004-2009) responsible for financial sector and the new commissioner with the same competences, Michel Barnier.

The EU financial legislation itself has two main aspects. On the one hand, it creates the new “European Systemic Risk Board”, which will warn about threats to financial stability. Its main members will be the 27 central bank governors in the EU member states, as well as the president and vice-president of the European Central Bank.

Separately, there will be a new “European System of Financial Supervisors”, which will oversee individual banks and financial firms.

Day-to-day supervision will remain with national supervisors. However, three existing pan-EU co-coordinating committees will be upgraded into new European Supervisory Authorities for the banking, insurance and securities sectors respectively.

These changes will develop harmonised rules and common approaches to supervision. Nevertheless, they will also ensure “consistent application” of the rules, and be able to co-ordinate and take some decisions in emergencies.

A fund for Eastern European banks

In the middle of January 2010, the first so-called "bad bank" for Eastern Europe was set up in the Austrian capital of Vienna. It has initially been allotted funds totaling around $250 mln, but is expected to receive a much larger sum – $1,5 bln from the World Bank, World Socialist Web Site reports.

The Deputy President of the International Finance Corporation, a subsidiary of the World Bank, Lars Thunell, which set up the fund, justified the move by pointing out that Eastern Europe was one of the regions that had been hardest hit by the worldwide financial crisis.

The bank has two purposes: first, its priority is to protect West European banks from defaults on billions of euros of loans (e.g. recently declared by the German Bavarian State Bank) by centralizing toxic assets and other securities in the new "bad bank". Second, freed from the burden of such bad loans on their balance sheets banks would once again be able to trade and freely take part in corporate financing.

The "toxic assets" will be exchanged on the basis of a decreased book value for debenture bonds. Banks with large bad loans on their balance sheets, which until now were denied fresh capital from central banks, will now be able to submit their debenture bonds with central banks as security for new credits. The whole circus of highly speculative and profitable financial speculations that led to the financial crisis in the first place can recommence, as if nothing had happened.

The role of the newly created bad bank is now to redeem the toxic credits that had been largely written off by major banks. It is no coincidence that the new bad bank is to be located in Vienna. On January 26, Austrian Financial Market Authority co-chairman Helmut Ettl announced he expected "massive write-offs" by Austrian banks in the coming year. Austrian banks have the largest exposure to Central and Eastern Europe, with substantial amounts of foreign-currency-denominated assets (particularly mortgages) in Hungary, the Czech Republic, Croatia and Slovakia.

The entire "bad bank" operation is aimed above all at rescuing Western European banks at any price and will do nothing to assist the hard-hit populations of the states in Eastern Europe. Success for this operation, however, remains extremely questionable. All of the calculations involved depend on a recovery from the deep economic recession in Eastern Europe economies. The reality is that in many states the economic situation is very slowly becoming better.

So far, the International Monetary Fund has been forced to intervene to provide financial help for Hungary, Romania and Ukraine in order to prevent the collapse of their economies. The latest prognoses for the region are not very optimistic.

During the past two years, Latvia's economy shrank by more than 24 per cent and, according to the IMF, the country's gross domestic product will decline a further 4 per cent in 2010. Estonia's total indebtedness amounts to 140 per cent of GDP and is only exceeded in the EU by Romania, with 160 per cent. Baltic States are estimated to have the highest levels of toxic assets (14.5%) followed by Estonia (12%), Romania (11.2%) and Bulgaria (10.1%), as well as in Lithuania and Hungary. With the economic downturn set to continue in these countries in 2010, the levels of these bad loans are also set to rise.

An additional factor for creating such a bank is rapidly rising unemployment, which in turn increases indebtedness of individual consumers. Unemployment in Eastern Europe is already clearly higher than in the west, and this difference will continue to grow. The number of Eastern European countries with an official unemployment rate of more than ten% has grown in the past few months.

Latvia has the highest official level of unemployment at 22 per cent, while double-digit jobless rates exist in Poland, Hungary, Slovakia, Slovenia, Serbia and Croatia. According to figures from the First Bank AD Novi Sad, unemployment in Serbia will rise from the current 16,5 per cent to 18,5 per cent in 2010. At the same time, such official unemployment figures invariably tend to underestimate the real situation. Taking into account underemployment, the real unemployment rates are likely to be much higher.

Numerous banks’ services

In the history of the global financial crisis the role of EU governance and Ms. Neelie Kroes, the former EU’s competition commissioner (2004-2009) in particular will be remembered; the latter set a welcome precedent at the end of October 2009 making some troublesome too-big-to-fail institution shrink. This move was in strict contradiction to the US-like approach looking like a Titanic designer arguing that the provision of extra lifeboats would solve the problem.

Some experts suggest a logical division between the main players in the financial aspect of the crisis: the retail banks, investment banks and asset managers, including private equity and hedge funds, which is more like a three-way split into utilities, casinos and people who visit casinos to gamble. Some politicians and regulators have argued that modern-day finance is too complex to be divided and those who suggest such divisions are being simplistic. But a three-way split would be easy enough to implement given the will.

Gapper J. A three-way split is the most logical. -Financial Times, October 29, 2009.

This mix of two-way or rather three-way split reveal most conflicts of interest and systematic problems in the businesses of what many too-big-to-fail institutions contain.

First, there would be retail banks, gathering deposits and using them to lend to individuals and small and medium-sized businesses. Such institutions, like the old UK clearing banks, would be tightly regulated, operate boringly and predictably, and be bailed out if necessary.

Second, there would be corporate banks, which would offer advisory, capital-raising and underwriting services to large companies and investors. Like traditional US investment banks, they would fund themselves independently without the backstop of a retail balance sheet.If they ran into trouble, they would be allowed to fail, argued J. Gapper. Such banks would have to operate with much less leverage, more capital and greater balance sheet liquidity than at the height of the financial bubble through sheer market forces; otherwise they could not fund themselves.

One problem of investment banks is that their employees have an incentive to take risks with capital for which they are not paying the full cost. Then investment banks would be forced to halt pure proprietary trading and divest their asset management arms. Everything from management of mutual and hedge funds to private equity would be done independently.

It would create an asset management sector in which large firms could co-exist with hedge fund managers and even proprietary trading desks.

These institutions could take whatever risks they chose with investors' money, provided they were honest about it; the governments would know that these gamblers would bear their own losses.

European Recovery Plan: new approaches to financial supervision

According to the Commission’s initiative, the Larosière Group was created in November 2008 in order to prepare a report to clarify the financial problem in Europe (further, Group). The report issues in February 2009 served a great deal in creating large consensus among professionals and political leaders, as well as in the European Council on the ways to regional recovery, including financial sector.

In approaching the crisis, most urgent was regarded a set of reforms in financial sector with adequate financial supervision. These reforms would be undertaken in concert by the EU institutions and the member states. Although the financial and banking sectors are generally regarded as being regional and even international in development, the banks every-day activity is mostly subject to national regulations.

The Commission’s President and two former commissioners in 2004-09 Commission (Joaquin Almunia and Charlie McCreevy) underlined that the main problem with what the Larosière group proposed was how to move faster with the reforms in order to introduce the new system in the EU already in 2010, rather than in 2012.

Important to mention, that these proposals are also forming major part in the European Economic Recovery Plan. The technical aspects of the plan are complicated but the fundamental issues are simple. As soon as financial markets are mainly outside the national reach, the EU must show collective political will to tackle future systemic risks before they get out of control.

More efficient financial supervision

At the “macro-level”, the Group’s envisaged a European Systemic Risk Council, which will assess risks to the stability of the European financial system as a whole. At micro-level, the new European System of Financial Supervisors will enhance supervision of individual cross-border financial institutions.

The Commission’s idea was not to impose “centralising of power” and taking away the role of national supervisors. The idea was rather to create a partnership between national supervisors and new European Supervisory Authorities; the latter based on existing EU Committees of Member State supervisors working in line with the “European concept” and real European interests.

In order to provide for easier lending for companies, impaired assets must be removed together with the recapitalization and restructuring of banks. The EU measures, according to the Commission, such as capital requirements, credit ratings agencies, hedge funds and private equity would help re-establish confidence and restore the demand for credit. But those measures can only work fully if they are complemented by a more effective architecture for financial market supervision that reflects modern reality, underlined J.-M. Barroso, Commission’s President.

The Commission wants Europe to be the first to implement its G-20 commitments on cross-border supervision. Having first mover’s advantage will show the G-20 partners that the EU expects them to go ahead with the same speed and determination. It will maximise Europe's influence in developing the global financial accounting system.

Improving supervisory cooperation

The idea of supervision has been on ECOFIN Council’s agendas for more than a decade; though, a very little progress has been achieved, argued the then Commissioner McCreevy.

It was expected that the present crisis would have spurred the member states and financial supervisors to find better ways of cooperation. But the crisis, the commissioner said, has had an opposite effect, i.e. it has reinforced the tendency for supervisors to think nationally.

Finance ministers in the member states did not get appropriate information on situation in the foreign owned banks on their territory; neither had the authorities in the member states any intention to inform other supervisors or finance ministers about decisions they were taking which could affect the banks operations in other member states.

The Commission’s decision to set up the De Larosiere group was the only right way to move this debate forward; the group’s report has provided the catalyst to take discussions onto a new level.

The proposals are aimed to equip the Single Market with a new and comprehensive system to preserve financial stability. This intention was to create a system based on two prudential control pillars, i.e. for micro and macro supervision.

As to the micro prudential level of supervision, the new system would be composed of 3 new European Supervisory Authorities: the European Banking Authority (EBA), the European Insurance and Occupational Pensions Authority (EIOPA) and the European Securities Authority (ESA). These would replace the three main current EU Committees of Supervisors (CEBS, CEIOPS and CESR). The new Authorities would be working in a network with national supervisors. This network would develop common supervisory approaches to the supervision of all financial firms, to protect consumers of financial services and to contribute to the development of a single set of harmonised rules. The new European Supervisory Authorities should draw up technical standards, help ensure the consistent ECOFIN application of Community law and resolve disputes between supervisors.

Maintaining 3 authorities, the Commission (based on the De Larosiere’s report) has envisaged the creation of a coordinating or steering group among the three Authorities. This over arching committee would have as its function ensuring consistent supervisory approaches, strengthening cooperation as well as addressing cross-sectoral challenges including financial conglomerates.

A critical issue is the “dispute settlement” mechanism, which aims to balance home and host interest in an effective financial supervision; the latter would not directly impinge on the fiscal responsibilities of the member sates. It would rather relate to issues concerning the organisation of supervision, the technical implementation of prudential rules and balanced information sharing between home and host financial authorities.

In crisis situations, the new Authorities would have a strong coordinating role, i.e. they should facilitate cooperation and exchange of information between competent authorities, act as a mediator when needed, verify the reliability of the information that should be available to all parties and help the relevant authorities to define and implement the right decisions.

The competences of the new Authorities would also include full supervisory powers for some specific financial entities (e.g. Credit Rating Agencies); the aggregation of all relevant micro-prudential information emanating from national supervisors; and a certain role in the EU activities at the global level, mainly with regard to technical aspects.

De Larosier’s recommendations were formulated in such a way that the proposals would not need changes in the basic Treaty. This was a pragmatic approach designed to work in the context of the current Treaty provisions and Court of Justice’s jurisdiction.

Financial problems turning into economic: Greek’s example

Budget deficits have exploded as tax revenues dried out in most European states; in addition, they poured extensively to stimulate citizens’ demand. The cost of the crisis is testing the investors’ patience to buy government bonds, when the latter are not fully solvent.

Such EU countries as Portugal, Ireland, Greece and Spain are trying to convince investors that they are able to close the deficit, e.g. Greece economy (due to inappropriate accounts) was reported down by only 1,2 per cent in 2008. However, after detailed scrutiny, it was seen that the government’s budget started 2009 with a deficit of 7,7 per cent that reached 12,7 per cent in February 2010. The country’s public debt has reached 120 per cent of national GDP in January-February 2010.

The Greek government’s recovery plan, agreed in the beginning of February with the European Commission, expected to reduce the deficit to 2 per cent by 2013, the aim sounded dubious to experts. No other state in the EU combines massive public debt, yawning deficit and unstable economy. Thus, Greek 10-year bonds were in February 2010 at 6,7 per cent, or about 2 percentage points higher than in Ireland or Portugal, the two other risky states in the eurozone.

Such instability inevitably provides negative affects on business in these countries; besides, local and foreign investors become frightened. Risk-averse investors will then race to drop exposed bonds, shares and other sovereigns, spreading crisis through other states.

In the mid-February 2010, the growing anxiety about sovereign risk led to sell-offs across Europe. The dollar hit a recent high against the euro of $1.36, and equity indices fell across Europe.

The European Commission promised to keep Greece’s economic development under scrutiny; it recommended Greece to invite International Monetary Fund experts having greater experience in these issues in order to arrange funding that will prevent a greater crisis.

If the crisis does deepen, Europe should be avoiding bailing out its own states. Bond market discipline failed during the boom as investors ignored the possibility of eurozone states running into trouble. If the EU rescues Greece, those days will return, and an important fiscal disciplining device for eurozone countries will disappear.

Most economists are of the opinion that if a rescue is needed, the IMF is the right body to organise it. It would impose tough conditions on the country that the EU would find hard to do. This would be embarrassing for European investors; but the bond market is a tough place to play.

Popular pressure on politicians to impose additional financial scrutiny and control on banks produced strong effect in the EU member states.

Role of banks in the Greek’s rescue plan

Because of poor tax collection, there is a growing government’s debt used to cover public needs. Public finances have been out of control: government debt reached 125 per cent of GDP, the highest in the Union (with 60 per cent limit in eurozone). The public sector has become unmanageably big and inefficient.

The money to cover public debt comes from both the EU member states’ financial institutions, mainly banks (as well as from other countries) and through EU subsidies.

As to the former, Greece is fully indebted to its eurozone’s fellow-members. Thus, according to Bank for International Settlements (the so-called central bank for world’s central banks), Greece owes to international lenders about 220 bln euro out of total 300 bln Greek government debt. The Greek banks own only 40 bln of the assets. Remarkable, of all Greek bond emissions during last decade only about 30 per cent was allocated domestically (almost a quarter was taken by the UK and Ireland); the rest is still in the “hands” of France and Germany. No wander the leaders of these two states govern the rescue package for Greece.

The biggest exposures to the crisis are mostly sovereign and private investors from France –about 60 bln, Switzerland –about 50 bln and Germany –about 43 bln; small share belongs to the US –12 bln, the UK- about 10 bln and Holland –9 bln. Some of these countries directly own local banks in Greece, e.g. French Credit Agricole and Societe General or German Deutsche Bank.

As to the Union’s assistance, Greece received since its adhesion to the Union billions of euro in regional, cohesion and other EU funds.

Financial reform is going on

The financial sector played a double role during last decades. On one side, it was one of the main driving forces for the EU growth since the creation of the single market in the early 90s. On the other side, this sector nearly caused the economy to collapse at the turn of 2008. The EU reforms would equip the EU institutions for the first time with a pan-European macro-prudential supervision system.

As to macro-prudential supervision, the Commission proposed a new body, the European Systemic Risk Council to ensure macro financial stability in the EU. Based on appropriate analysis, the Council would be able to detect potential threats to the stability of the entire European financial system and, if needed, to issue early warnings about these threats and make recommendations to avoid them.

In doing so, the EU will be able to ensure that the member states escape from the boom-bust dynamic that is at the origin of the systemic failures that have characterised the functioning of the pre-crisis European financial system.

The President of the European Central Bank would chair the Systemic Risk Council; and the ECB would play a key role in its functioning. Its members would include all the central bank governors of the 27 Member States, the Vice-President of the ECB, the chairpersons of the 3 new European Supervisory Authorities and a member of the European Commission. This composition reflects the links between micro- and macro supervision and the necessary consistency between these authorities and the Commission.

It is important that the judgments made by the Council are based on information of the utmost quality. Therefore, the access to information is a key issue and it is crucial that the warnings and recommendations are followed by action. This new authorities would, obviously, be in close contact with the IMF, the Financial Stability Board and other international systemic-risk counterparts.

Business and banks: access to finance

SMEs are the backbone of the European economy, representing about 67-70 per cent of regional employment (compared with 55 per cent in the US). Large companies also depend on SMEs as suppliers and manufacturers. At a time of crisis, the banks reduced the credits to small companies. However, the EU member states’ financial institutions and banks received billions of euros of government assistance from recovery funds, but they remain reluctant to lend (see the table below).

Access to finance for SMEs is limited to the banks; the latter are more risk avers. The hardest times for SMEs are probably still lie ahead, as they hand in the balance sheets to banks.

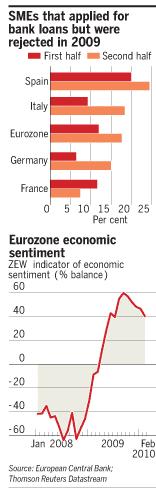

Difficulties for SMEs in obtaining finance have intensified in the eurozone’s 16 states too. Rejections of bank loan applications rose significantly in the second half of 2009 compared with the previous six months, a European Central Bank survey of SMEs showed, with Spanish companies worst hit. Access to finance was cited as their most pressing problem by 19 per cent of those surveyed – up from 17 per cent previously.

Atkins R. Europe’s SMEs face funding difficulties. –Financial Times, 17 February 2010, p. 4.

It adds to evidence that a weakened banking sector is constraining economic growth, with the effects of the global financial crisis still feeding through into individual lending decisions. The larger role played by bank loans in the region, especially for SMEs that cannot raise funds from capital markets, makes the eurozone more vulnerable to loan drought then in the US.

Some experts see that the economic recovery in Europe is losing momentum. Germany’s ZEW economic institute reported its “economic sentiment” indicator for Europe’s largest economy had declined for a fifth consecutive month. However, the German’s ZEW index – regarded as a useful indicator of likely trends in economic activity – was still significantly higher than its historical average.

“Although we have passed through the deepest valleys of the depression, worries about the labour market, budget deficits and the euro have not lessened,” said Wolfgang Franz, ZEW president in Financial Times (17.02.2010). Last week, gross domestic product data showed the eurozone economy expanded just 0.1 per cent in the fourth quarter of last year, with Germany stagnating. Looking ahead, German economic activity could “move sideways, with only minor ups and downs”, Mr. Franz added.

The ECB launched a survey of the SMEs financing conditions for the end of 2009. It showed that in its first half, 77 per cent of SMEs had received in full or part the bank loans they had sought, as a sign that credit was continuing to flow into the real economy. However, in the second part, that figure deteriorated to 75 per cent. Moreover, the share of SMEs bank loans’ refusal rose from 12 per cent to 18 per cent.

Among the large eurozone countries, the rejection rate for loan applications rose from 6 per cent to 15 per cent in Germany, and from 9 per cent to 18 per cent in Italy. But the rate was highest in Spain, where it rose from 20 per cent to 25 per cent. In France, the rejection rate fell from 12 per cent to 7 per cent.

The general picture is such that about 20 per cent of eurozone’s SMEs expected access to bank loans to deteriorate in the first six months of 2010, compared with only 14 per cent expecting an improvement.

The literature on the EU financial and economic issues can be found at: http://ec.europa.eu/economy_finance/publications/economic/index_en.htm

US bank “revolution”

Interesting initiative appears from the US, so-called “Volcker rule”, a proposal from the EU Presidential administration. But real changes that are taking place in the US are much more fundamental, often called the US bank revolution.

These changes are covering both financial and economic guidance, i.e. for the first time in the country’s history an economic recovery board of advisers is established in the President’s administration, with Mr. Paul Volcker as its chairman (former chairman of the Federal Reserve). His proposals are mainly of two dimensions: first, splitting banks from proprietary trading (so-to-say, a commercial bank can not perform simultaneously investment functions), and second, none of the banks can be “that big” as to take acquire a considerable share in the national economic structures.

The effect of the proposal is a dramatic effect for the American financial sector: e.g. main US banks, for example Goldman Sachs or JP Morgan Chase should give up their bank status if they want to avoid the ban on proprietary trading. The two mentioned groups are, at the same time, financial holding companies and as such has the right to borrow money from the Federal Reserve and accept retail deposits.

Besides, the US idea of creating Consumer Financial Protection Agency has been of interest both in the US and internationally.

«The Baltic Course» Is Sold and Stays in Business!

«The Baltic Course» Is Sold and Stays in Business!