Banks, Estonia, Financial Services

International Internet Magazine. Baltic States news & analytics

Thursday, 25.04.2024, 21:45

Estonian banks earned profits of 4 bln kroons in 2008

Print version

Print versionIn Estonia the total volume of banks' loan and leasing portfolio grew by 7.3% in 2008. The total portfolio volume increased by 18 billion kroons during the year, amounting to 269 billion kroons.

As a result of a decline in credit demand caused by economic adjustment and tightening lending conditions, the stock of loans and leasing to enterprises and households dropped by 2.3 billion kroons, i.e., 0.9%, in December. A majority of the decline derived from the repayment of loans granted to trading sector enterprises. In December, the volume of new housing loans turned out smaller than the repayment amount of earlier loans, thus the mortgage loan portfolio decreased by approximately 200 million kroons.

|

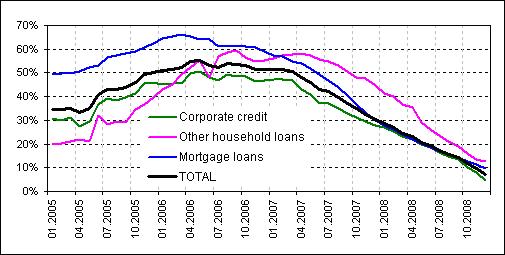

| The annual growth of household and corporate loans and leases in Estonia |

Risks to the Estonian banking system arising from credit market constraints due to the international financial crisis are mitigated by smaller credit demand and household saving. Since the economy is adjusting, credit demand will remain modest throughout 2009.

In December the deposits of Estonian households and non-financial enterprises increased by 2.1 billion kroons, i.e., 2%, amounting to 106 billion kroons. Owing to the annual increase in deposit interest rates, the share of households' and enterprises' time and saving deposits has grown, standing at 60 per-cent and 41%, respectively, at end-December. Saving has also been encouraged by future uncertainty. Although the contraction of international money market interest rates is starting to impact the interest rates on kroon deposits, households and enterprises expectedly keep accumulating savings into their bank accounts.

|

|

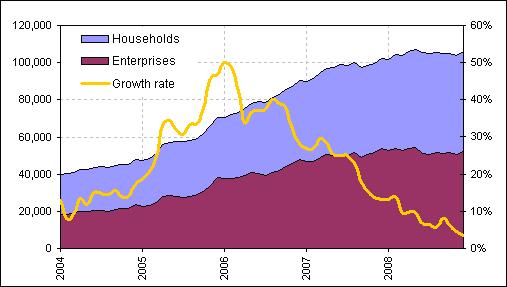

The volume of corporate and household deposits (EEK million) in Estonia and the annual deposit growth rate |

The average capital adequacy of banks amounted to 18.8% in December and has been substantially above the required 10% level throughout the past six months. In 2008, banks operating in Estonia earned approximately 4 billion kroons as net profit. This was nearly 50% less than in 2007, but still a tenth higher than in 2006. The net profit of banks was reduced by loan write-downs, which amounted to 1.9 billion kroons, i.e., to 0.8%, of the loan portfolio in 2008.

The share of loans overdue by more than 60 days increased from the November 2.5% level to 2.9% by end-December. This was in line with the projected result of changes in the economic environment and does not threaten the reliability of banks. The share of overdue loans is the biggest in the property and construction sectors as regards enterprises and, in the case of households, in the segment of consumer credit. These three sectors in the aggregate make up over a half of the loans overdue for more than 60 days. The high capitalisation of banks enables them to cope even in the case of possible higher loan losses.

In coming months, the monthly loan repayments of borrowers will decline owing to the falling interest rates in the international money market. As key interest rates fell, the average interest rate on new housing loans and long-term corporate credit issued in December dropped to 5.4% and 5.8%, respectively. Thus, the interest rates on new loans have declined to the level of mid-2007. Since the euro-area money market interest rates continue to decline, the retail interest rates will decrease further and the interest repayment amounts of earlier borrowers will also be smaller.

|

|

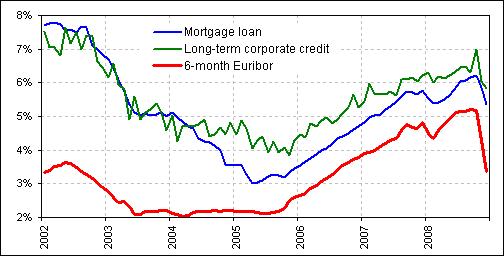

The weighted average interest rate on housing loans and long-term corporate loans issued within a month and the 6-month EURIBOR |

«The Baltic Course» Is Sold and Stays in Business!

«The Baltic Course» Is Sold and Stays in Business!