Banks, Estonia, Financial Services, Loan

International Internet Magazine. Baltic States news & analytics

Saturday, 20.04.2024, 08:53

Bank profits decreased somewhat in the second quarter in Estonia

Print version

Print versionThe value

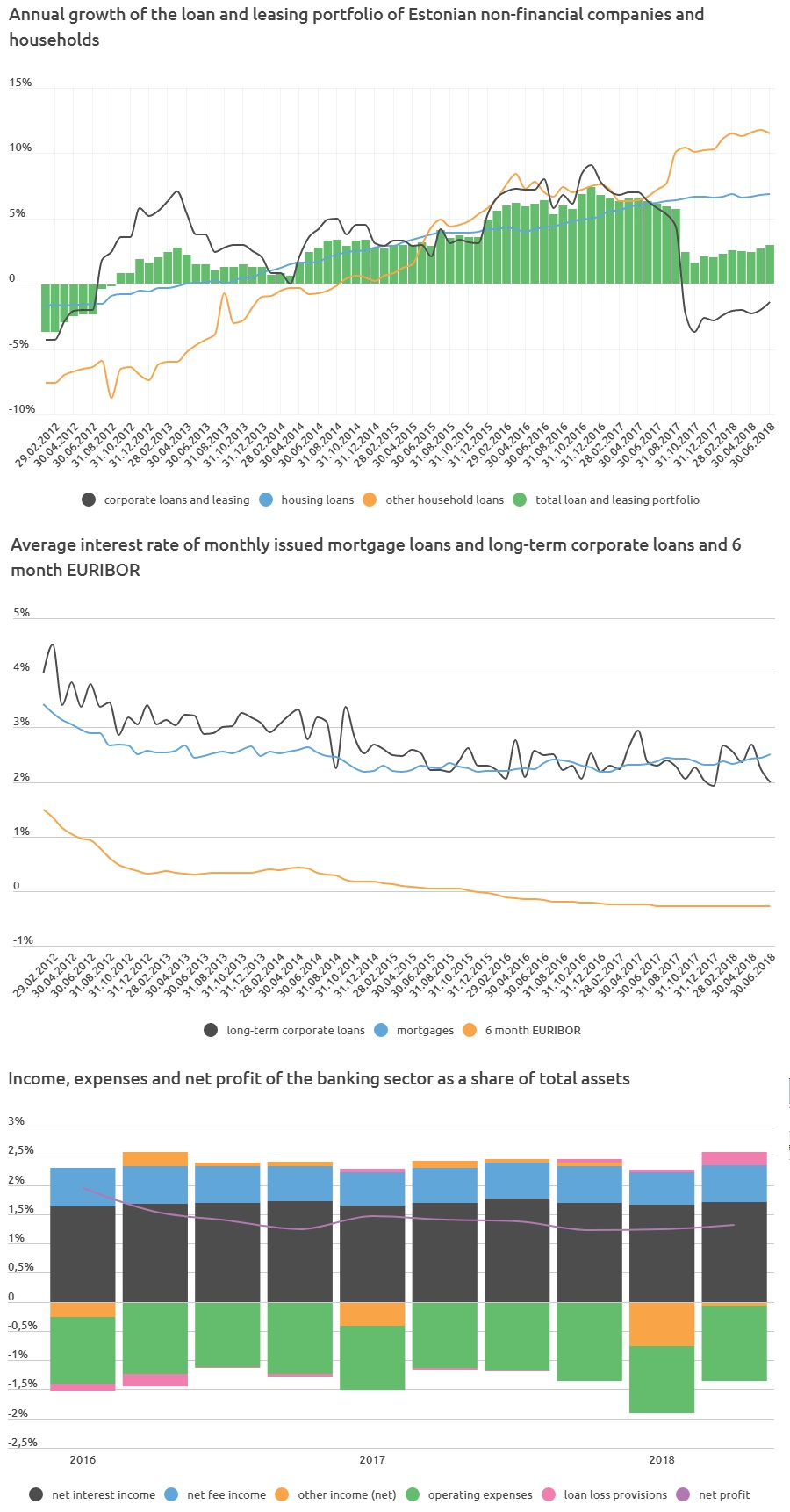

of new car leases signed in June was 30% more than a year earlier, and the

annual growth of the car lease portfolio reached 20%. The annual growth of

other consumer loans was also rapid at almost 9%. The fast increase of consumer

loans reflects both the current favorable economic environment and increased

supply. Consumer loans and leases make up around one fifth of the total loan

and leasing portfolio of households.

The stock

of housing loans grew in June at around the same rate as it had in previous

months. 117 mln euros’ worth of new housing loans were taken out,

which was 12% more than a year earlier. The growth stems from higher-priced

real estate and larger average loan sums, but also from the fact that more

transactions were made. The annual growth of the housing loan portfolio has

been close to 7% over the past six months.

Corporate

loan growth has been more moderate than household loan growth due to low

investment activity. However, companies’ loans from banks operating in

Estonia did increase in the second quarter. The stock of new loans grew in all

major sectors compared to the year before, and the increase of the loan

portfolio has been relatively homogeneous.

The average

interest rate for new housing loans has risen somewhat since the start of the

year, reaching 2.5% in June. Despite being the highest level of the past

four years, it can still be considered low long-term. The average interest

rate of new corporate loans largely depends on the kind of companies that sign

loan contracts over a specific period and the kind of projects they undertake,

and it can therefore fluctuate quite a lot. In July, it was down to 2%.

The

deposits of Estonian households and companies grew rapidly alongside active

borrowing. The stock of deposits held by banks increased by almost 12% or

13.8 mln euros in a year.

The net

profit of the banking sector fell a bit in the second quarter of 2018. The

net profit of the quarter was 82.5 mln euros in total, which was 3% less than

in the previous year. At the same time, net interest income rose by almost 3%

year-on-year, mostly thanks to smaller interest expenses. Service fee income

increased, as did wage costs and administrative costs. One-off factors boosting

profit were the reversal of previous provisions, and dividends from

subsidiaries. As a result of the new income tax rules that took effect at

the start of the year, banks calculated around 8 mln euros for income tax

expenses in the second quarter.

«The Baltic Course» Is Sold and Stays in Business!

«The Baltic Course» Is Sold and Stays in Business!