Analytics, EU – Baltic States, Financial Services, Investments, Markets and Companies

International Internet Magazine. Baltic States news & analytics

Thursday, 18.04.2024, 11:19

German companies in the Baltic States perceive slight economic upward trend

Print version

Print versionThe worldwide economic downturn had strong effects on the Baltic States in the past two years. Estonia, Latvia and Lithuania were notably affected by the global financial and economic crisis and suffered a considerable contraction of their GDP. With negative growth rates of 14.1 percent (Estonia), 18.0 percent (Latvia) and 15.0 percent (Lithuania), the three Baltic States experienced the hardest economic recession among all EU member states. However, since the end of 2009, a stabilization and even upswing can be noted. While the economic downturn slowed down significantly in Latvia, Estonia and Lithuania have already recorded even a slight growth of their seasonally adjusted GDP data in the fourth quarter of 2009. Economic recovery is expected to continue in the course of the current year and will lead to a return to growth in 2011 at the latest. The growth rates will not reach the level of the pre-crisis years but will put the economies on a generally more solid and sustainable ground.

German companies perceive first signs of recovery

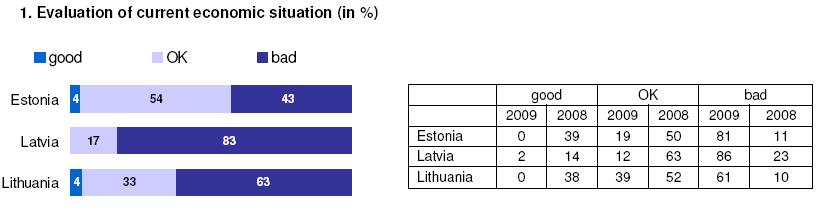

First signs of recovery are also traceable in the perceptions of German companies regarding the prospective economic situation in the Baltic States. In spite of the rather critical assessment of the current situation, they show considerably more optimism than last year. Although only 2 percent of the companies perceive the current macroeconomic situation as good, 19 percent foresee an improvement for the course of 2010. In addition, the number of respondents who expect a further stabilization of the macro economy has increased substantially as compared to 2009. However, nearly two thirds still characterize the present situation as bad. In pan-Baltic comparison, the situation in Estonia is seen as being better than in Latvia and Lithuania. Differences also exist between sectors: Uncertainty prevails especially in the prospects of companies from the building and construction sector, while the responses from the trade and service sector reflect mixed feelings about the development in current year. A clear upward trend is expected in the manufacturing sector: No single company predicts a further decline and worsening of the situation in its respective sector.

Cautious optimism for the own business

The economic downturn also affects the activities of the German companies. Contrary to previous years, they could not defy the general market downturn anymore and had to cope with noticeable downturns in sales. Over 60 percent of the respondents reported lower turnovers and profits in 2009, thus confirming their pessimistic forecasts from last spring’s survey. In addition to low domestic demand and limited export possibilities to other markets, negative developments regarding payment behaviour of business partners and an increasing number of insolvencies have also negatively affected their balance sheets. German companies thus are presently rather sobered with respect to the current situation of their own business activities. However, their own companies` situation is considered to be better than the overall economic situation – as was the case in previous surveys as well. With more than a fourth of the respondents characterizing the situation of their company as good, the positive evaluations still slightly outnumber the negative ones. For the future, the prospects are more promising. 40 percent of the German companies expect an improvement of their business situation in the coming years. More than one third anticipates a growth in turnover and profits already in 2010 – with the biggest optimists being located in Estonia which the German companies on site expect to be the first Baltic country emerging from the recession.

Investments remain strategically long-term oriented

The rather confident future expectations of German companies are also reflected in their investment and employment plans. After having adapted to the current economic situation by reducing investment and implementing necessary structural adjustments in 2009, the majority of the respondents are ready to increase investments in the current year. More than two thirds intend to keep their investments at least at the same level as last year or even plan to increase them in order to stabilize their operations in the Baltic States and to strengthen or improve their market position. At the same time, several German companies that are not yet active in the Baltic States are intending to enter the markets. Their aim is to start their activities in the current phase of consolidation in order to build a basis for mutual advantageous commercial partnerships in the next growth period. This clearly indicates that German companies are basing their decisions not on short-term turnover aspects but rather following their own long-term strategy and business plans.

German companies foster investment and employment

The volume and inflow of German investments remains steady even in current economically difficult times. German investments in the Baltic States lay at 40 million EUR in 2009 and amounted to a total of 1.7 billion EUR by the end of the year. Germany is thus one of the biggest investors in Estonia, Latvia and Lithuania with 6 percent of total foreign investments. Additional investments have been made by daughter companies and branches of German companies located in third countries. The number of German companies operating in the Baltic States is currently estimated to be around 2 000. German production and services operations have become an integral part of the Baltic economies and foster prosperity and employment in Estonia, Latvia and Lithuania by providing and securing jobs – both directly and indirectly. Vice versa, the number of Baltic companies in Germany is also increasing continuously. A total of 118 companies from Estonia, Latvia and Lithuania were registered in Germany by the end of 2009 – most of them are active in the wholesale and in the service sectors.

Foreign trade less dynamic but still intensive

Besides the mutual investment activities, Germany and the Baltic States traditionally have very intensive trade relations. After a very dynamic development in the last years, the German-Baltic trade decreased in 2009 due to the general decline on the worldwide commercial markets caused by the financial crisis and the economic slowdown. Compared with 2008, the trade volume between the Baltic States and Germany went down by 28 percent to 5.3 billion EUR in 2009. Germany’s exports to the Baltic States dropped by 37 percent to 5.3 billion EUR, while imports went down only 3 percent to 2.0 billion EUR. The trade deficit of the Baltic States was thus reduced considerably compared to the previous years and amounted to 3.3 billion by the end of 2009. Germany still remains one of the most important trade partners for the Baltic States. Building on this solid basis the economic cooperation will continue to grow. Despite the currently rather tense economic situation in Estonia, Latvia and Lithuania, there is still demand for German products and services. This is expected to further increase once more with the on-going recovery and get close to the pre-crisis level seen in the medium term. At the same time more and more companies from the Baltic States are targeting the German market and intensifying their export activities. Due to domestic demand contraction, the interest in Germany as Europe’s biggest market has increased steadily in recent years. Being one of main target countries, Germany has managed to move up several positions in the ranking of the export partners – irrespective of the slight decrease of export of goods and services to Germany in the last year. In addition to the increasing export activities of local companies, there will be further bilateral trade impulses by the German companies on site. After a lower demand and fewer exports in 2009, about 90 percent of the respondents expect to be able to further raise their exports or at least stabilize them at the current level – regarding exports both to Germany and other markets.

Positive signals on employment and labour market

Even in economically challenging times, German companies in general are still financially stable and offer their employees high job security – both in Germany and the Baltic States. This is to be seen in the entrepreneurial decisions in the human resources field: 60 percent of the respondents intend to keep the number of their employees at the current level. Another 20 percent are planning to employ new personnel. They can benefit from considerably lower labour costs and a higher number of qualified workers available on the labour market. Compared to last year, the motivation and productivity of employees has also improved. Despite these positive developments, especially the rigid labour legislation and the quality of the vocational education system continue to be a barrier for doing business. In order to be able to react adequately to market changes, German companies demand a greater flexibility of the labour legislation and a more practice-oriented professional education. The existing vocational education system is seen as inappropriate and should be reformed to better suit the requirements of the companies. The respondents also recommend active labour market measures to tackle the notably rising unemployment and the migration of the workforce.

Crisis management of the governments is only partly convincing

German companies not only stress an immediate need for policy action on the labour market but also a series of measures to be taken by the respective governments to stabilize the national economy. To respond effectively to current cyclical dynamics and the macroeconomic situation, the governments of the three Baltic States are asked to use their limited financial resources for supporting the export industry and stimulate investment activities. However, the trust in the governments’ ability to cope with the crisis is rather limited. A mere 20 percent of all respondents assess the measures already taken to overcome the financial crisis and tackle the recession as satisfactory and target-oriented. Only in Estonia the steps initiated by the government rather meet the expectations of the German companies. Here, more than in Latvia and Lithuania, German companies in Estonia have also been in a position to take advantage of the existing governmental programmes – especially of employment guarantees and export support schemes. For 20 percent of the respondents in Estonia, however, the programmes are not available or unknown. In addition, only a relatively small number of the respondents take into consideration to make use of the governmental programmes at all. This indicates that in all three countries the conditions for the use of such programmes are either not attractive enough for the companies or not well enough communicated by the governments.

Economic policy remain in the focus of criticism

Bigger emphasis has to be put on economic policy. It should follow a clear long-term strategy and reduce barriers and obstacles to investments and doing business in the Baltic States. In times of great economic uncertainty, companies need to operate in a stable framework which offers reliable parameters for their entrepreneurial decisions. Economic stability and political predictability are thus of outmost importance. From the entrepreneurial perspective the in some cases rather short-notice modifications of the tax system did not result in sufficient transparency and legal certainty. Especially the German companies in Latvia and Lithuania voiced their dissatisfaction with changes in the tax system and the tax burden. Governmental organisations and institutions are requested to improve the competitiveness of the Baltic economies and to create conditions for a stable and sustainable economic development. Constant targets of criticism are the unsatisfactory prevention of and combat against crime and corruption as well government services which often appear to lack efficiency and service orientation. Other aspects being considered as problematic by German companies are the lack of transparency in public tenders and the limited access to public and EU funds.

Strong call for the Euro

German companies further stress the need for an on-going consolidation of the government debts as wells as a limitation of budget deficits. With regard to the intended introduction of the Euro by 01 January 2011 in Estonia, these two aspects are of special importance here: all German companies active in Estonia strongly support joining the Euro-zone. In Latvia and Lithuania 83 percent of the respondents are also in favour for the introduction of the common European currency which is expected at a later stage than in Estonia. The number of Euro-advocates among German companies is thus as high as never before. The Euro is a clear sign of trust and increase confidence by ultimately ending the latent discussion of the devaluation of the national currencies. It would provide some security in difficult economic times caused by a global financial and economic crisis that hit all markets. Considered to be a solid and stabilising factor in currency markets, the access to the Euro zone could have a positive impact on the rating of the Baltic economies and the business activities of the companies – both inside and outside the European Union. By becoming members of the European monetary union, the Baltic States will also be the most integrated countries in northern Europe. If Estonia joined the Euro zone by 01 January 2011 as intended, it would be the first and only country in the region which is member of the European Union, NATO, Schengen, and the Euro zone. The same perspective is seen by Latvia and Lithuania who are both planning to introduce the Euro by 01 January 2014. The different target dates of the three governments for becoming member of the European monetary union are also reflected in the expectations of the German companies about the date they hope to take advantage of the Euro. While in Estonia 82 percent of the respondents predict that the Kroon will be replaced by the Euro in 2011, the majority of the companies in Latvia and Lithuania expect 2014 to be the earliest date for the euro introduction.

German companies are committed to Estonia, Latvia and Lithuania

The introduction of the Euro will improve the investment climate in the Baltic States and make them more attractive for foreign investors - even though without the Euro the three economies are also already considered attractive business locations. Despite the significant economic downturn and more critical assessment of certain conditions for doing business, 86 pct of the German companies would repeat their engagement in the three countries. This result once more confirms the long-term orientation of German investors who are not reacting mechanically to recent downturns in sales by cutting investments or relocating their activities. Estonia, Latvia and Lithuania are rather viewed with a long-term strategy and German companies still have confidence in the markets. Only a few investment decisions might have been reconsidered by the respective company – mainly because of a high dissatisfaction with the public administration, changes in the tax system, and a critical assessment of the legal certainty and the combat against corruption. These aspects of the business environment thus could not only have a negative impact on present business but also need to be improved to avoid hindering future investments in the Baltic States.

Estonia, Latvia and Lithuania remain attractive for German businessmen

In comparison to other Central and Eastern European countries – as well as Germany and China – the Baltic States still enjoy a high attractiveness for German companies. Among the countries in the Central and Eastern European region Estonia had the best results and reached second place behind Germany which was top in the ranking of the most attractive business location for the second time in a row. Germany has continuously improved its competitiveness and can profit from a trend to investments on stable markets in current uncertain times. Lithuania, last year ranked fifth, dropped to rank eight as several other countries are expected to be better business locations by the respondents. Besides Germany and Estonia, neighbouring Poland has become more attractive for German companies active in Lithuania. Being the only country in Central and Eastern Europe that managed the crisis without negative growth figures, Poland also improved in the overall ranking and reached the third position. Latvia has remained on ninth place among a total of 21 locations assessed in the survey. This is mainly due to the critical external assessments from German companies active in the neighbouring Baltic countries as respondents in Latvia only consider Germany to be a possible alternative business location.

Summary: German investors still assess their engagement in the Baltics positively

The Baltic States are still attractive business locations for German companies. Despite the criticism regarding certain factors affecting their business activities and perceived difficulties, German companies still consider Estonia, Latvia and Lithuania to be good markets for their economic activities. The financial and economic crisis has not caused any doubts regarding their past investment decisions and the vast majority would thus repeat their engagement in the three countries. This proves the thorough planning and elaboration of investment decisions which allow German companies to trust in their own strength and competitiveness even in the current crisis. It also proves that German companies are not driven by short-term cost or turnover aspects but rather following a long-term strategy. By doing so, they play an important role for the stabilization of the Baltic economies.

«The Baltic Course» Is Sold and Stays in Business!

«The Baltic Course» Is Sold and Stays in Business!